The future of financial services will be defined by data—and by who can act on data most effectively. For credit unions, the move toward data-driven finance is not new, but what is changing is the scale and speed at which data can be used. Advances in artificial intelligence are shifting the industry from incremental progress to a new paradigm, where insights can be generated and acted on in real time. Data remains the foundation of nearly everything being built in the modern digital world, yet it is still one of the most underutilized assets within credit unions. In this new phase, becoming data-driven will look very different than it has in the past. As agents become more capable, they will increasingly operate across every aspect of the credit union—from internal workflows to external member journeys.

Traditionally, data lived inside core systems and flowed outward through scheduled reports rather than directly into action. Insights were periodic, decisions were manual, and analytics functioned as an input to leadership rather than an engine of execution. That model is now giving way to a more dynamic approach, where data flows freely across systems, intelligence is accessible to more people, and insights can be translated into action in near real time—often with the support of intelligent agents embedded within workflows.

This shift toward data-driven finance is about building foundations that allow data to move, combine, and flow into better processes and outcomes. It positions credit unions to respond faster, operate with greater precision, and personalize more deeply. As these capabilities mature, agents can begin to operate alongside people to continuously monitor data and execute tasks within defined processes. The opportunity is to move from reporting on the past to shaping the future—using data not just to inform decisions, but to power them.

Core Systems and Reports: The Traditional Data Model

Core systems are the system of record for nearly all credit unions, and this model has worked reasonably well for decades. Data flows into the core, transactions are processed, and balances are maintained. But core systems are built with highly predefined structures optimized for operations, not flexible analysis. Integrating additional data sources—such as digital interactions, richer payments data from card networks, or external context—is often difficult, and access to usable data depends heavily on the tools exposed by the core provider. As a result, working with core data can feel like interacting with a slow, opaque black box.

Given these constraints, most credit unions rely on reports as their primary form of business intelligence. Business analysts translate questions into SQL queries, dashboards, or spreadsheets. Sometimes this works, but more often it becomes an iterative back-and-forth. Requests queue up, analysts become bottlenecks, and decision-makers face delays. In practice, some teams move forward without the data because waiting for the report feels more costly than acting without it.

This model has clear limitations. Data is fragmented and difficult to combine across domains. Reports are static and backward-looking. Even when insights emerge they rarely connect directly to action, and someone still decides what to do and executes through separate processes. The challenge is not that credit unions lack data, it is that data remains siloed, mediated, and slow to activate.

Building the Foundation for Intelligent Agents: Warehouses, Lakes, and Lakehouses

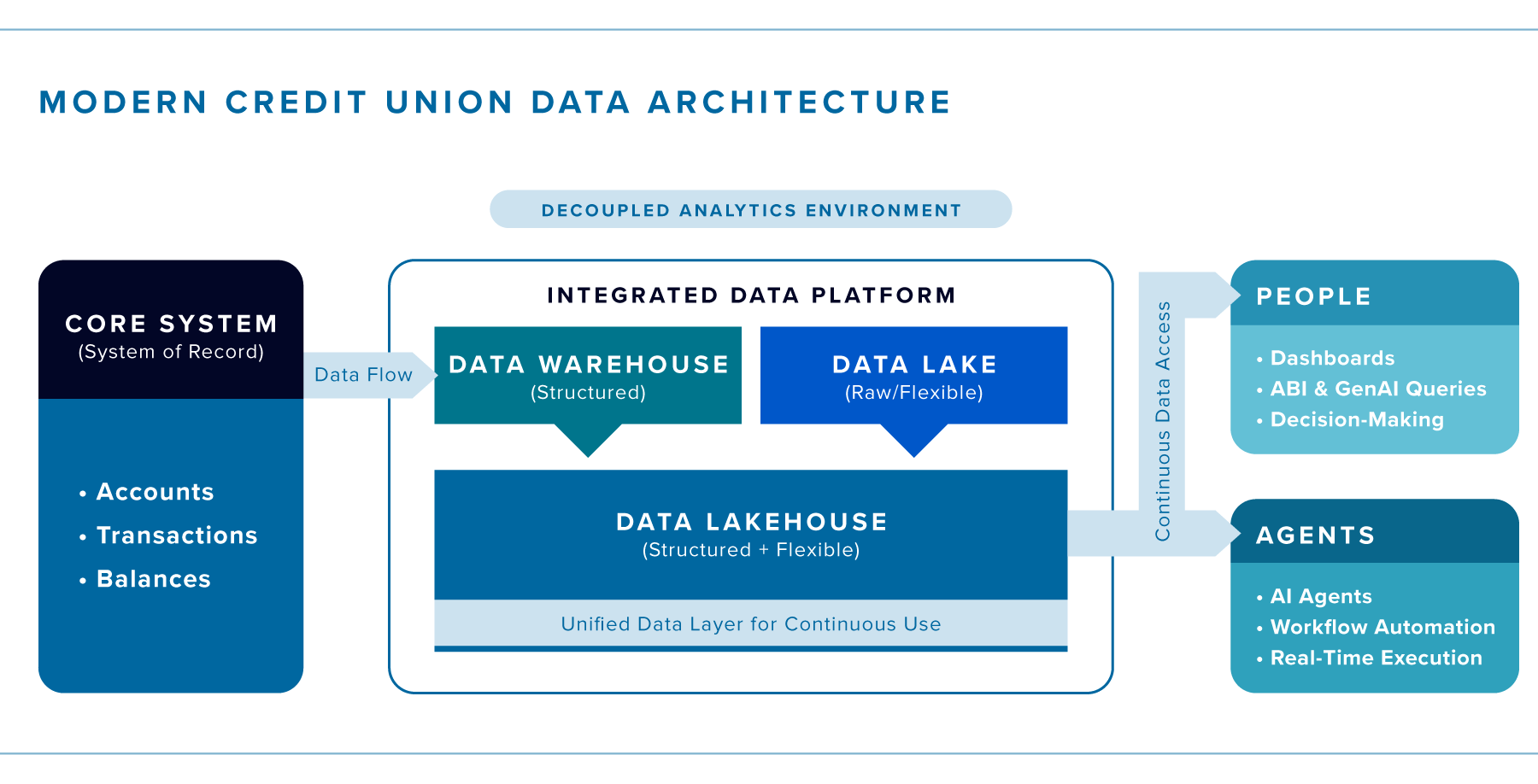

The shift to data-driven finance begins with modern data architecture. Over the past decade, credit unions have invested in data warehouses, data lakes, and more recently, data lakehouses. Some institutions are early in this transition, while others are further along. Prior research from Filene, including work by Dr. Cheri-Pero, has outlined the importance of building a modern data stack to unlock analytics value. What matters most is why this foundation is becoming essential for the future. As finance moves toward real-time intelligence and agent-driven decision-making, credit unions need data environments designed not just for reporting, but for continuous use by people, models, and machines.

Building the Modern Credit Union Data Stack to Leverage Analytics Value: Key Investments and Partners

This report introduces the modern credit union data stack and describes key capabilities and partnerships that will support credit union efforts to thrive into the future.

Modern data architectures serve complementary roles. A data warehouse stores structured, curated data optimized for analytics and reporting. A data lake provides flexible storage for raw structured and unstructured data (e.g., from documents or call-center transcripts). A data lakehouse combines the governance and performance of a warehouse with the flexibility of a lake. While the terminology matters less than the outcome, the strategic shift is clear: analytics are being decoupled from the core. The core remains the system of record, but day-to-day work with data increasingly happens in platforms the credit union controls.

Decoupling from the core addresses both the data constraint and the analytics bottleneck. Credit unions gain a transparent environment where data can be integrated, combined, and accessed more freely. When properly governed, this broader data foundation allows institutions to understand member behavior from multiple perspectives, improving insight into intent, risk, and opportunity. With data more accessible, analytics no longer depend on a small group of specialists; business intelligence can extend across the organization and prepare credit unions for more advanced, AI-driven decision-making.

From Business Intelligence to Artificial Business Intelligence (ABI)

Artificial intelligence is changing how organizations work with data. Traditional business intelligence relied on dashboards and reports that summarized what had already happened, often placing distance between questions and answers. Insights were mediated, delayed, and disconnected from the moment decisions needed to be made. Generative AI collapses that distance by changing who can work with data and how quickly understanding emerges.

The shift can be understood as a move from traditional Business Intelligence to Artificial Business Intelligence (ABI)—a model where business users interact directly with institutional data through generative AI. Instead of relying on spreadsheets or specialized SQL skills, leaders and staff can ask questions in plain English and explore scenarios conversationally. Through iterative prompting and response, users clarify intent, test assumptions, and refine questions in real time.

Consider a simple example. An executive using a tool like Microsoft Copilot might ask, “How did member growth change last quarter?” Follow-up questions could explore which segments drove growth, where momentum slowed, and what actions might improve performance in the current quarter. What once required multiple reports and meetings becomes a continuous dialogue with the data.

The value of ABI becomes clear in everyday credit union workflows. Leaders can explore loan pipeline performance, identify emerging credit risks, or analyze deposit trends without waiting on new reports. Frontline teams can better understand member behavior, personalize service interactions, and respond more effectively in real time. Across functions—from lending and marketing to operations and risk—ABI shortens the path from question to insight.

ABI removes friction between curiosity and understanding across the entire organization. It democratizes data access, empowering everyone—from leadership teams to frontline staff—to integrate data into daily workflows and decisions. When people can engage data simply by asking a question, data becomes a living part of how the organization thinks and acts.

From Insight to Action: Data-Driven Processes and Agentic AI

As data becomes more accessible and intelligence more conversational, the next evolution is action. Data-driven processes integrate analytics and AI directly into workflows, enabling decisions to be evaluated and executed in real time. Rather than stopping at insight, these processes use live data to trigger tasks, route work, and adjust outcomes continuously, turning analytics into a core component of day-to-day operations.

For decades, analytics focused on producing actionable insights. The prevailing model assumed humans would always sit between insight and execution—interpreting reports, weighing options, and manually initiating next steps. As data volumes increased and decision cycles accelerated, this approach struggled to scale. Data-driven processes address this limitation by embedding intelligence directly into how work moves through the organization.

This shift creates the conditions for agentic AI. Agentic systems do more than analyze data or generate recommendations; they continuously monitor conditions, evaluate context, and act within defined boundaries. Within data-driven processes, agents route tasks, trigger workflows, adjust parameters, and escalate decisions when human judgment is required. They operate as persistent participants in workflows rather than tools invoked on demand.

An Agentic AI Primer for Credit Unions

For credit unions, this fundamentally reshapes how work gets done. Instead of data flowing into reports and meetings, intelligence is embedded directly into operations. Many business processes begin to resemble a flow between two actors: a human and an AI agent. Monitoring, pattern detection, and routine execution are handled by agents, while humans step in where judgment, context, accountability, and member relationships matter most. Leaders remain responsible for strategy and oversight, but execution becomes faster, more consistent, and more scalable.

In practice, this can take many forms. Internally, agents can monitor loan pipelines, flag emerging risks, rebalance call queues, reconcile transactions, and adapt fraud controls in real time. Externally, an agent can recognize changes in a member’s spending patterns, surface timely insights, and proactively engage the member with personalized recommendations like a savings product or loan. Leaders remain responsible for strategy and oversight, while execution becomes faster, more consistent, and more scalable.

The result is an in-line process where data powers intelligent workflow automation across the institution. Decisions are no longer episodic or constrained by reporting cycles; they are continuous and adaptive. This allows credit unions to scale efficiently without losing control, increase speed without sacrificing judgment, and respond to member needs in real time rather than after the fact.

The true breakthrough is the ability to continuously act on data as part of every business process. Leadership shifts from a reactive mindset to a proactive focus on improving how decisions are made and executed. As agentic systems take on lower-level execution, people gain the capacity to focus on direction, design, and member impact. When data-driven processes and human judgment work together, credit unions can adapt continuously and compound their effectiveness.

Conclusion

Data-driven finance is no longer about faster reports or better dashboards. It is about building systems that allow data to move freely, intelligence to emerge naturally, and action to occur continuously. Artificial Business Intelligence lowers the barrier between questions and answers. Agentic AI closes the gap between insight and execution.

Credit unions have the opportunity to elevate how work gets done by combining modern data architecture with AI agents that unlock the full potential of their data. Data becomes the resource, and agents apply that resource across workflows and decisions. As routine execution shifts to agents, leaders can focus more fully on what matters most for the credit union and its members: deepening relationships, delivering more personalized value, and reinforcing long-term trust. In this future, data is a strategic asset, and intelligent agents become the amplifiers that shape how the institution thinks, acts, and adapts over time.