Buckle up, because the times are changing. We have lived through decades of digital transformation, yet most financial services still rely on data systems built 50 years ago. Everything, from core systems to the card networks, runs on legacy infrastructure. We are now living through a true paradigm shift in these systems—one that will redefine how value moves, how assets are managed, and how work is automated. This shift matters because it has immediate implications for payments, liquidity, and operational efficiency. If today’s credit union leaders get this right, they will create lasting impact for their members.

This shift matters because it has immediate implications for payments, liquidity, and operational efficiency. If today’s credit union leaders get this right, they will create lasting impact for their members.

Everyone is familiar with crypto and AI as emerging technologies, but did you know there is a common theme underpinning them? These innovations can feel like two distinct trends, yet understanding one key concept will help you unlock the next level—the “token.” We are shifting toward an economy built on tokens, which spans everything from stablecoins to AI. A token is the new language for units of value and information. Stablecoins process units of money as a token. AI processes units of words as a token. Once you see this parallel, the connection becomes clear. This is the future of finance, because this is how we’ll process both value and information.

To tokenize something is to convert it into a standardized digital form that can be programmed, transferred, and automated. The term “tokenize” ties together everything we are seeing in these emerging trends. It is not just the underlying technologies of blockchain or large language models. It is a mindset shift in the way that we think about value and information. This shift has profound implications for the future of finance.

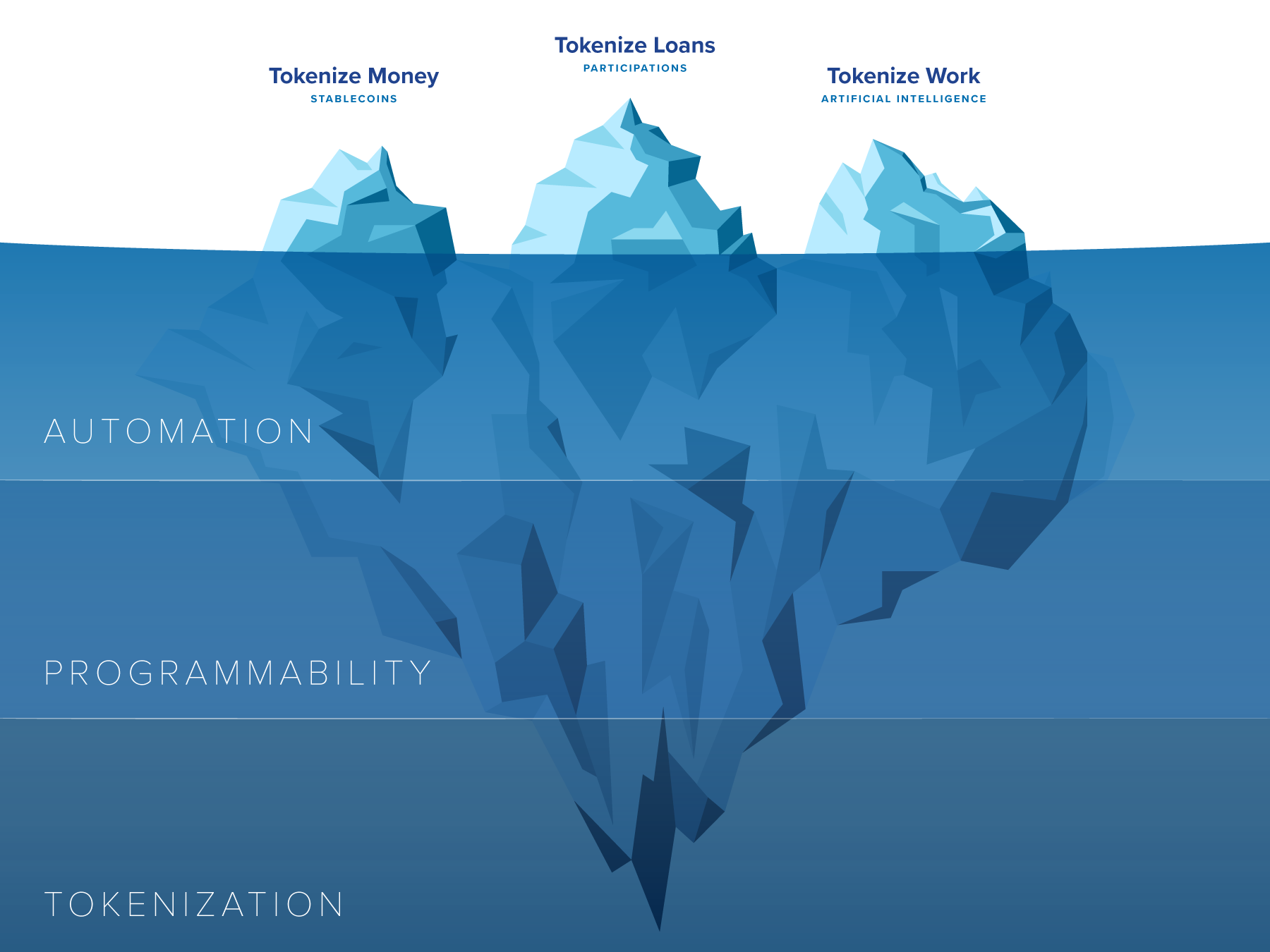

What does it mean to “tokenize finance”? We’ll look at three emerging applications to help illustrate the idea: stablecoins that tokenize money, loan participations that tokenize loans, and artificial intelligence and how it can tokenize work. Think of these applications as the tips of an iceberg. On the surface, distinct and unrelated. But beneath is a shared foundation: value and information turned into standardized digital units—tokens—that can move easily across systems. This foundation represents the paradigm shift underway across financial services. Stablecoins turn dollars into programmable, real-time digital units of value. Loan participations will turn a world of brokers and third-party databases into shared, dynamic digital contracts. Artificial intelligence tokenizes work by turning knowledge and decisions into programmable digital units that can be processed, automated, and analyzed.

Tokenization holds a significant deeper benefit across all three applications—it enables programmability and automation. With value and information in the form of standardized tokens, code can act on them. Stablecoins become digital dollars that can be processed by smart contracts to automate transactions. Future loan participations as tokenized loans will use smart contracts to record ownership and automate reporting and payments. AI agents will process tokens as units of information to analyze data and route tasks for intelligent workflow automation.

Taken together, these use cases reveal a future of finance programmed end-to-end—tokenization automating the movement of value, the verification of ownership, and the analysis of data. If the applications are the tips of the iceberg, then tokens form the layer just below the surface, programmability sits beneath the tokens, and automation is the deepest layer that gives the entire structure its power. Tokenization leads to programmability, and programmability leads to automation.

Tokenization is laying the foundation for the next generation of financial infrastructure, and credit union leaders have an opportunity to apply these innovations in ways that benefit their members. What sits below the surface today will soon define how we move money, manage assets, and automate work. The following three use cases—tokenizing money, loans, and work—are visible applications with accessible starting points for the leaders of tomorrow. I invite you to explore how your credit union can tap into these deeper layers of programmable and autonomous finance as you begin charting a path forward.

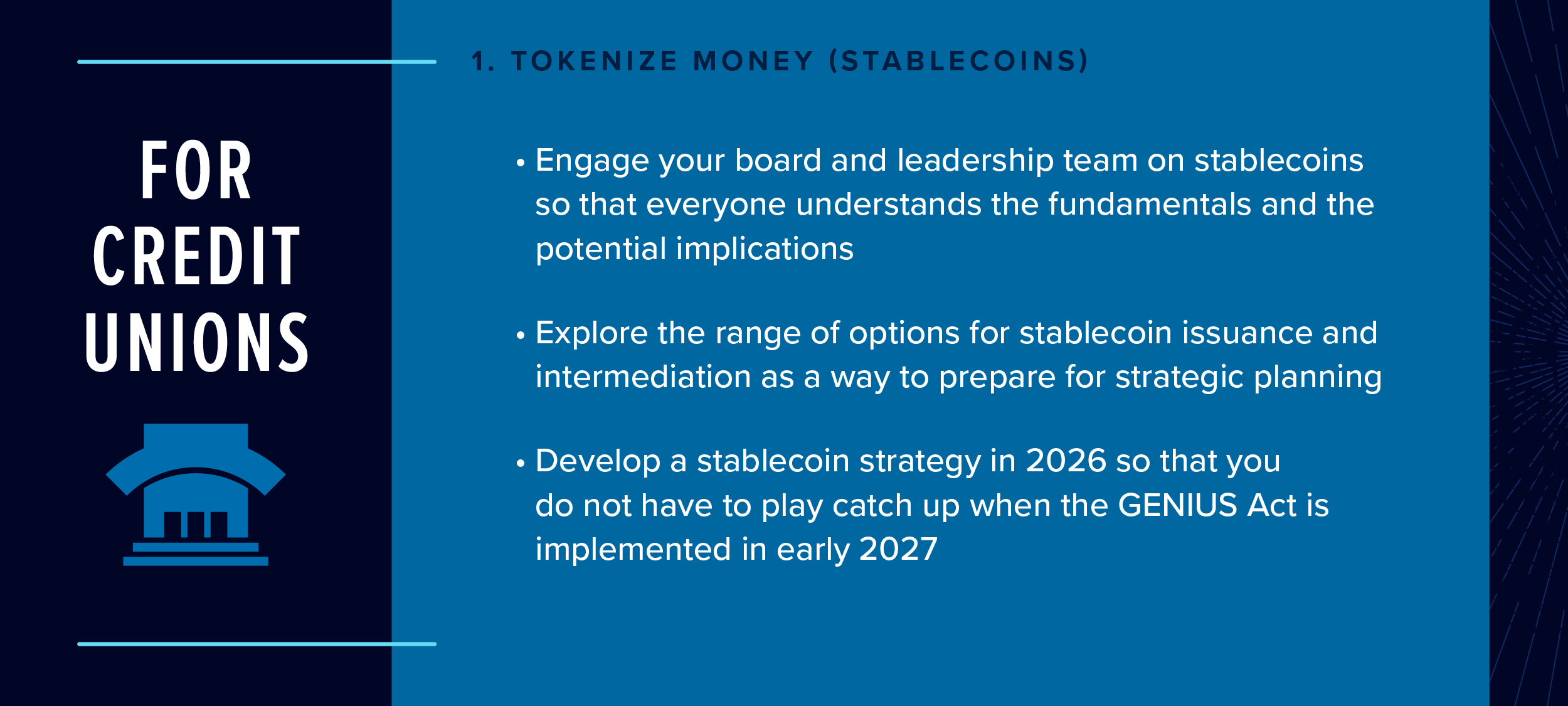

1. Tokenize Money (Stablecoins)

Stablecoins are tokens that combine the technology of cryptocurrency with the stability of traditional currency. By transacting on decentralized payment rails (i.e., public blockchains) while pegged one-to-one with the U.S. dollar or other fiat currency, stablecoins enable near-instant, programmable payments without reliance on card networks or correspondent banks. The passage of the GENIUS Act (July 2025), a federal law creating the first U.S. regulatory framework for payment via stablecoins, has accelerated discussion across the credit union industry about how stablecoins could redefine payments.

Stablecoins eliminate the need for traditional settlement and reconciliation because blockchain functions as the distributed ledger. This tokenization of money reduces friction while preserving the value of the dollar. The potential disruption to legacy payments is significant: faster settlement, programmable features, and broader accessibility could permanently shift consumer expectations.

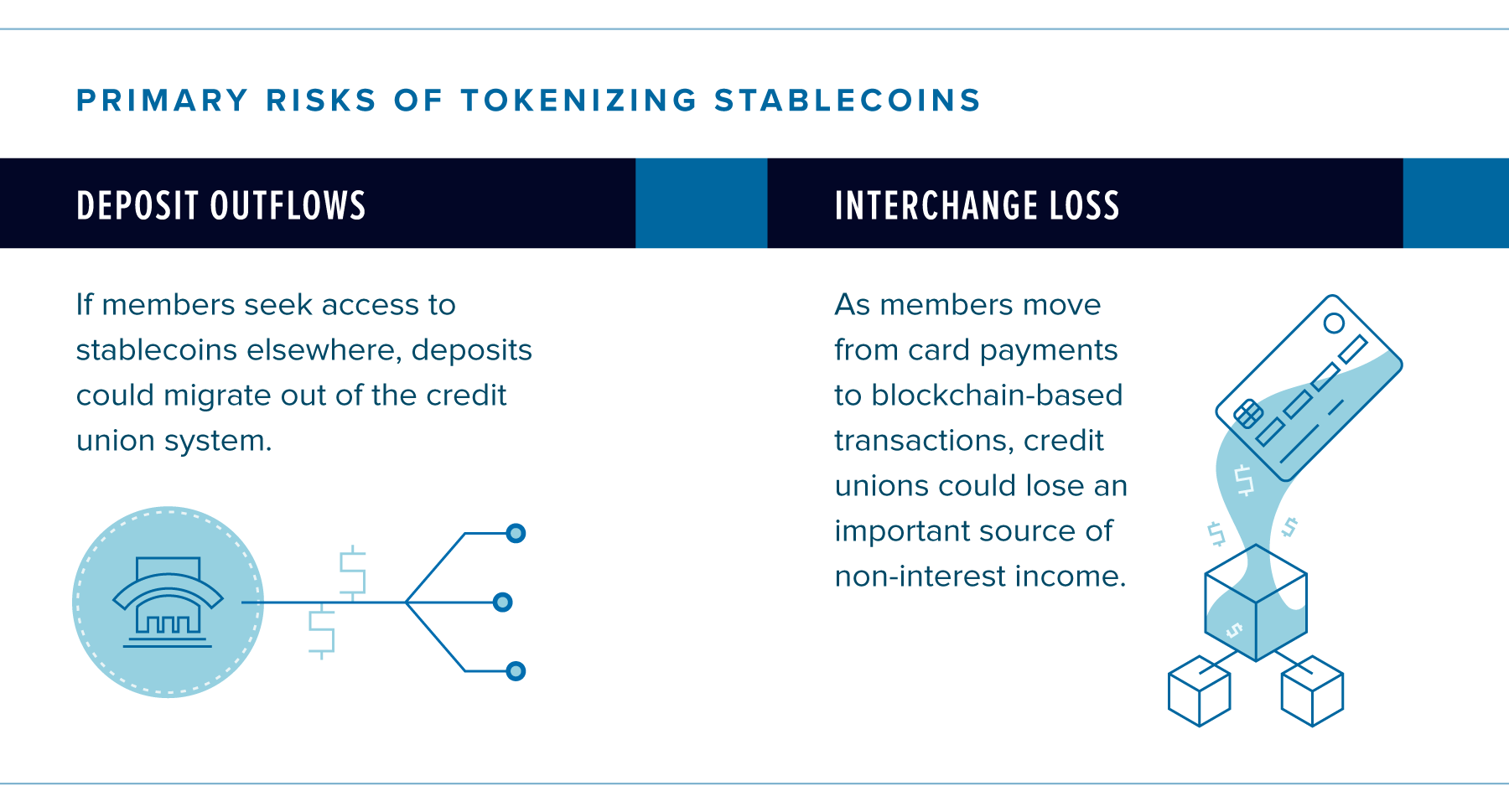

Credit unions face the strategic choice of whether to issue stablecoins or become an intermediary. With trade-offs to either choice, every credit union should weigh its decision carefully.

Issuing your own stablecoin could mean employing a single- or multi-owner CUSO that holds dollar reserves and issues a credit union-branded token. The benefits are branding, control over programmable dollars, and the potential to mitigate deposit outflows by internalizing members’ money. However, issuance involves significant operational investment, regulatory compliance, and the risk that the stablecoin is not adopted. Stablecoins depend on network effects; without broad usability for payments or transfers, even a well-designed token will have limited member value.

An intermediary strategy integrates existing stablecoins (e.g., USDC) into digital banking channels, enabling members to buy, store, send, and receive stablecoins through the credit union’s mobile app. The advantages are increased speed-to-market, lower investment cost, and minimal operational burden. The trade-off is reduced control and differentiation, since the credit union relies on a third-party issuer. This approach must therefore be developed with a strong emphasis on trust and security, both for members and in relation to the issuer itself.

Each strategy will require serious preparation as GENIUS Act rulemaking accelerates through 2026–27 and stablecoins become a mainstream exchange medium. Issuance is likely to make the most sense at the industry level, with a handful of CUSOs creating shared stablecoin infrastructure. For most individual credit unions, the key decision will be how to integrate these trusted stablecoins and design a seamless member experience as programmable and automated forms of money become the norm. The goal is to ensure that credit unions remain relevant participants in this paradigm shift toward the tokenization of money.

Credit Unions and the Quickly Changing Stablecoin Conversation

2. Tokenize Loans (Participations)

The same technology that enables stablecoins can also transform the loan participation market. Welcome to the world of tokenizing loans. If tokenizing money makes payments programmable, tokenizing loans makes ownership and servicing programmable. A loan is already a digital record stored in a core system, but that record lives in a closed database. Tokenization extends its utility by placing it on a shared ledger where ownership, participation, and payment functions can be managed transparently.

The term “digital asset” now extends far beyond cryptocurrencies like Bitcoin. Digital assets include tokens on a shared ledger that represent real-world assets like real estate, vehicles, or even stocks. Each token acts as a verifiable, transferable claim, creating decentralized ownership records that are transparent and secure. This means credit unions can leverage blockchain tokens to represent real-world assets (not just cryptocurrencies), opening the door to new ways of managing loans or collateral. The NCUA understands these benefits and issued guidance in 2022 that allows credit unions to apply distributed ledger technology in a safe and sound manner.

The most relevant application for credit unions is the tokenization of their primary asset—loans. Today, loans live inside core systems designed for balance-sheet lending, not for sharing or selling assets. In loan participations, where ownership must be divided and transferred, the process still relies on spreadsheets, emails, and manual verification. Tokenization replaces this fragmented approach with a single, shared source of truth—one digital contract that all parties access, update, and trust. Instead of circulating files and reconciling versions, participants interact with the same tokenized loan, where reporting of ownership, payment allocations, and servicing actions are updated automatically through smart contracts. This shift reduces friction, lowers operational risk, and creates a more liquid and transparent participation market.

Through FiLab’s support, our LoanNFT platform demonstrates how blockchain can streamline loan participations by minting loan pools as collections of digital tokens. This approach improves transparency, enhances data integrity, and shortens deal cycles between originators and funders. Tokenized assets could open secondary markets for loans that are often illiquid (e.g., ITIN or CDFI loans), allowing capital to flow more efficiently across the cooperative system. By lowering transaction costs and creating a shared data layer, tokenization strengthens liquidity and transparency, ultimately driving more value back to members.

Tokenized assets could open secondary markets for loans that are often illiquid (e.g., ITIN or CDFI loans), allowing capital to flow more efficiently across the cooperative system. By lowering transaction costs and creating a shared data layer, tokenization strengthens liquidity and transparency, ultimately driving more value back to members.

As this infrastructure matures, shared ledgers may become the new ledger for managing assets as programmable tokens. In this model, trust is distributed rather than centralized, and key servicing functions can be automated through smart contracts that update ownership, allocate payments, and verify data in real time. By turning loans into tokens, credit unions unlock a system where programmability drives automation, and where participation across institutions becomes faster, safer, and more inclusive.

Introducing LoanNFT, a Blockchain Solution for the Secondary Loan Market

3. Tokenize Work (Artificial Intelligence)

Tokenization is not limited to money or assets—it’s redefining how work itself is created, executed, and automated. With artificial intelligence, information is broken down into tokens, the smallest units of meaning that models can understand and process. Each token represents a fragment of data that can be recombined into insights, decisions, or actions.

This idea of turning complexity into standardized parts isn’t new. JSON (JavaScript Object Notation) was an early form of information tokenization that transformed messy data into structured, machine-readable objects. JSON made information portable and processable across systems like the internet. AI extends that same principle by decomposing human language and cognition into standardized tokens that can be measured, priced, sequenced, and used to train models.

As agentic AI matures, these systems will move beyond analysis to execution. Autonomous agents will negotiate services, perform tasks, and settle payments on behalf of humans and organizations. They will transact using stablecoins and other digital tokens as programmable dollars, enabling machine-to-machine commerce through automated micropayments.

This is the tokenization of work. AI will transform knowledge, decisioning, and execution into workflow automation. Each step, from data retrieval to task completion, becomes a tokenized unit of value that can trigger other actions automatically. For credit unions, this could mean AI agents that manage underwriting queues, verify identity documents, monitor compliance thresholds, or reconcile transactions in real time. Many credit unions already use basic AI for fraud detection and chatbots; the next phase will be autonomous agents operating behind the scenes as part of daily operations.

For credit unions, this could mean AI agents that manage underwriting queues, verify identity documents, monitor compliance thresholds, or reconcile transactions in real time. Many credit unions already use basic AI for fraud detection and chatbots; the next phase will be autonomous agents operating behind the scenes as part of daily operations.

Agentic AI will need to be governed by transparent guardrails designed to ensure safety, accuracy, and accountability. These guardrails can include human-in-the-loop oversight; policy-based controls that constrain agent behavior within defined risk limits; audit trails that ensure every action is traceable and reviewable; and segregation of duties, where agents handle routine or narrowly defined responsibilities while humans retain judgment-based authority. Together, these controls make automation trustworthy and align agentic systems with the credit union’s mission.

When both financial value and information exist as tokens, automation becomes granular, dynamic, and adaptive. For credit unions, this represents a new frontier where AI agents and tokenized workflows converge to reshape how operations run and how value is delivered to members. Work itself becomes programmable.

The Evolution and Impact of AI in Credit Unions

The Invitation to Tokenize

To tokenize finance is to prepare for a future where money, assets, and work exist as digital units that can be programmed, automated, and exchanged across institutions. Tokenization standardizes the units of value and information. Programmability amplifies what can be done with those units. As credit unions learn to apply these tools across end-to-end processes, this shift will unlock new levels of efficiency, transparency, and automation for members.

These trends may feel far away, but the momentum is already building. The GENIUS Act accelerated the move toward tokenizing the U.S. dollar, bringing stablecoins into the mainstream and introducing faster settlement and programmable features. Tokenized loans could unlock new efficiencies in the participation market with the automation of reporting, servicing, and payments. Meanwhile, AI agents are evolving from conversational assistants to autonomous actors capable of streamlining and executing workflows. With these changes converging, every institution will need to determine how it will interface with this emerging layer of programmable finance.

The credit unions that thrive in this next era will be those that experiment early while leaning into their strengths of trust, compliance, and a deeply rooted commitment to their members.

The credit unions that thrive in this next era will be those that experiment early while leaning into their strengths of trust, compliance, and a deeply rooted commitment to their members. Whether tokenized finance disrupts or transforms the credit union industry will depend on how, and how soon, its leaders choose to adapt to this new paradigm.