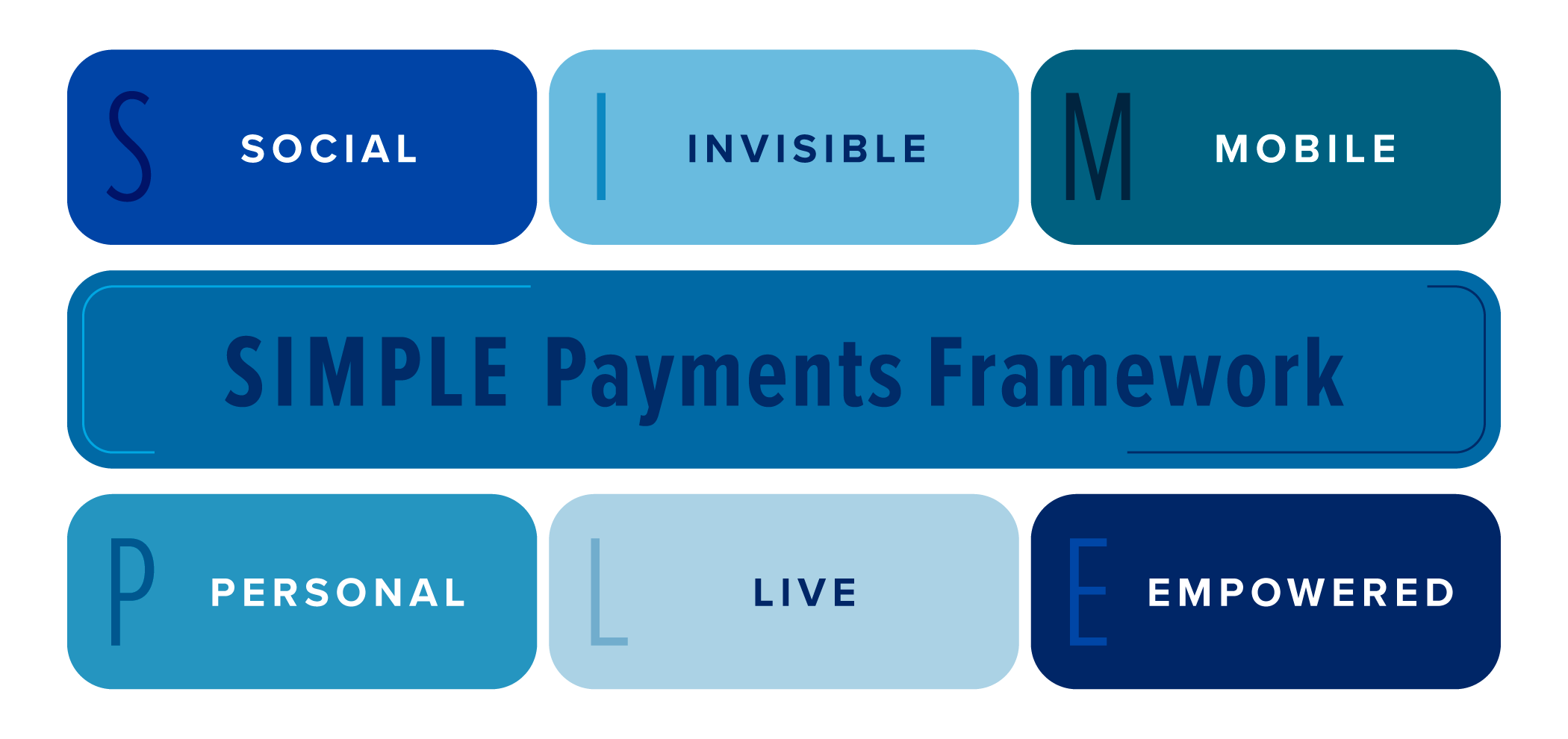

Consumer expectations around payments are shifting rapidly. As technology continues to advance, changes to payments are being fueled by mobile wallets, real-time experiences, and the seamless design of today’s most popular apps. For credit unions, staying relevant in this evolving landscape means understanding not just how payments work, but how people want to pay. To help credit union leaders navigate this change, I have developed the “SIMPLE Payments” framework: six key trends—Social, Invisible, Mobile, Personal, Live, and Empowered payments—that capture how consumer behavior is evolving and what it means for the future of member engagement.

Each trend represents both a challenge and an opportunity for credit unions to modernize their offerings and deepen relationships in a digital-first world. This article describes each trend and then provides actionable steps for credit union leaders who see the trend and want to adapt. If you can understand and evolve with these behavioral trends, you will stay relevant and competitive in an increasingly digital payments ecosystem. When you think about your credit union’s payments strategy, just think “Keep it SIMPLE!”

Social (S)

As digital communication continues to evolve, payments are becoming part of how people connect. Peer-to-peer (P2P) platforms allow users to split bills, send gifts, or request money directly within text messages and social media. Apps like Venmo have turned money transfers into a social experience complete with emojis, payment notes, and public feeds. Messaging tools like texts and Meta’s Messenger allow users to send or request money without ever leaving the conversation. With Apple Cash, moving money can be done with the tapping of two phones. These services blur the line between communication and commerce by making it easier to transfer funds as part of everyday life.

Usage of payment apps is increasing, especially among young people. A 2022 Pew Research Center survey found that 76% of Americans have used at least one peer-to-peer payment app, and particularly high usage among younger adults with 57% of 18 to 29 year-old report using Venmo.i A 2023 survey by Chase found that 64% of U.S. consumers used P2P services to send or receive money with friends and family, compared to just 22% who used cash,ii showing the shift from traditional methods to digital-first payments. The total value of peer-to-peer transactions in the U.S. is projected to reach $2.3 trillion in 2026, up nearly 13.5% from 2025.iii

In this new environment, payments aren’t just transactions, they are part of the social fabric. Friends often split dinner bills in the same thread where the dinner was planned. This means the boundary between financial tools and social tools is disappearing, and with it, the old model of logging into a separate app to complete a simple money transfer. Today, money is just part of the broader social sharing of messages with one another.

In this new environment, payments aren’t just transactions, they are part of the social fabric.

Ironically, this isn’t an entirely new phenomenon. In the earlier paper-based era, post offices served a dual purpose of handling both communication via letters and basic financial services like money orders. Today’s platforms echo that history, but with real-time digital capabilities and far greater user expectations. Today’s consumers, especially younger generations, expect to move money as easily as sending a meme or reacting to a message. Convenience, speed, and context are all part of the equation.

While innovating in the payments space can be challenging, especially with reliance on third-party providers, that doesn’t mean credit unions can just watch and wait from the sidelines. This trend toward social payments goes beyond deciding whether to pay for Zelle. The evolution signals a critical shift in how payment experience should be designed, with member experience at the center. It is no longer enough for payments to be secure and functional; they must also feel intuitive, social, and part of the natural flow of daily life. Even if the options for providers seem limited, credit unions that want to remain relevant must explore ways to integrate payments into the digital ecosystems where their members are spending their time.