No one needs to tell a credit union leader that new members aren’t going to flock to them because they offer a particular checking account or a loan or a credit card. Even “premium” features and products, such as high-yield savings accounts, have become commonplace and easily accessible for the average consumer. The ubiquity of deposit and credit products within financial services is a known challenge, but it is one that many successful organizations have solved for in ways that reflect their brand, value proposition, and differentiators.

Last year, Filene collected and analyzed key financial products offered by leading digital banks, national banks, and credit unions. We documented product name, tag line, elevator pitch, and rates and features for all consumer checking, savings, personal lending, auto lending, home lending, and credit cards, adding up to 271 products across 10 institutions. For each institution, we compared their product sets in terms of messaging, features, and experience. See Analysis Appendix for more details.

The high-level findings were unsurprising. The products, even in terms of features, are basically the same. What used to be differentiators have become table stakes.

When we dug deeper, we saw three successful strategies for differentiating products:

- Aligning products to specific identities or life stages

- Integrating products into broader financial ecosystems

- Emphasizing ease in consumer experience

Here’s how those strategies make products stand out in a crowded market.

Differentiation strategy #1: Aligning products to specific identities or life stages

Successful digital banks position their product portfolio in line with the overall market segment they are targeting. SoFi, for example, frames its products around ambition, momentum, and financial progress. The product portfolio is designed around consumers navigating financial advancement and major life transitions: career acceleration, higher education, homeownership, family formation, investing, and wealth building. The messaging consistently reinforces themes of “getting ahead,” career growth, investing in yourself, and building a better future. Its products are not simply marketed to younger consumers; they are structured around the financial realities and ambitions associated with upward mobility. The products are part of a broader identity narrative.

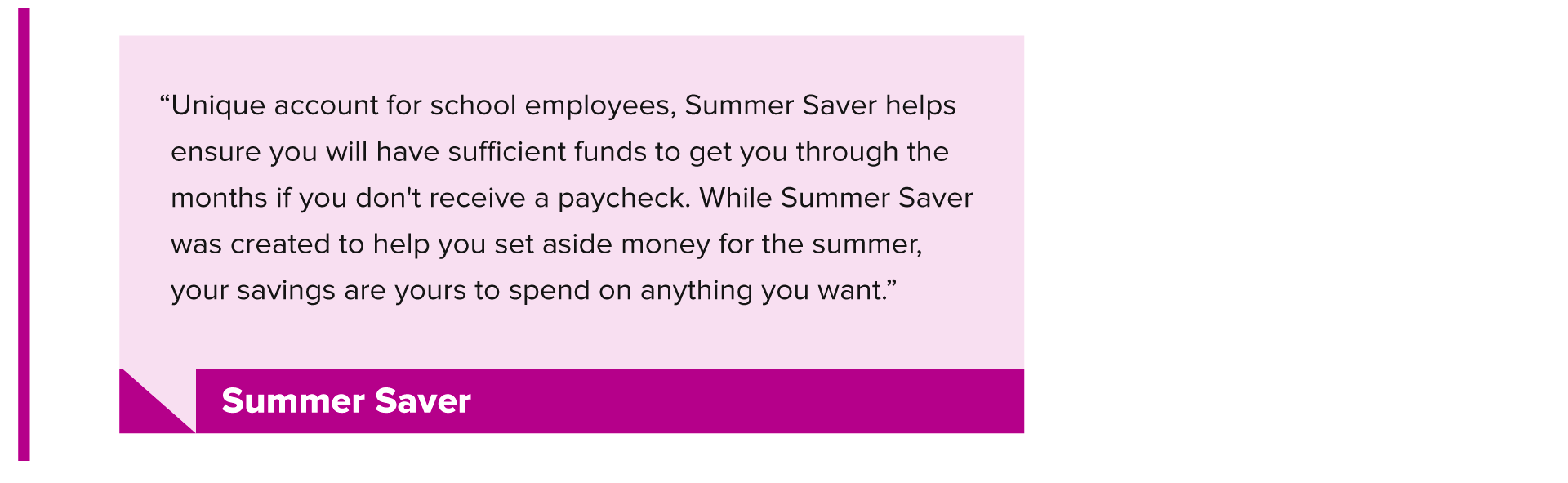

Rather than targeting a life stage, SchoolsFirst’s product strategy is centered around an identity: educators. Products like Summer Saver and School Employee Auto Loans are specifically structured around school-year cash flow cycles, summer income gaps, and classroom-related financial pressures.

The product immediately signals who it is for, what problem it solves, and that the institution understands the lived realities of its members. This becomes particularly important for younger consumers, who increasingly evaluate institutions not simply on product availability, but on whether the institution feels relevant, understandable, and aligned to their lives.

Differentiation strategy #2: Integrating products into broader financial ecosystems

Large national banks were the strongest examples of this ecosystem-based strategy incorporating their broader portfolios, sophisticated rewards, mortgages, cards, and digital tools to become the strongest features and rates competitors making the overall ecosystem feel valuable, integrated, and difficult to leave.

Their competitive advantage is less about offering dramatically different checking accounts or credit cards and more about creating integrated relationship models that become increasingly valuable as members deepen engagement across products.

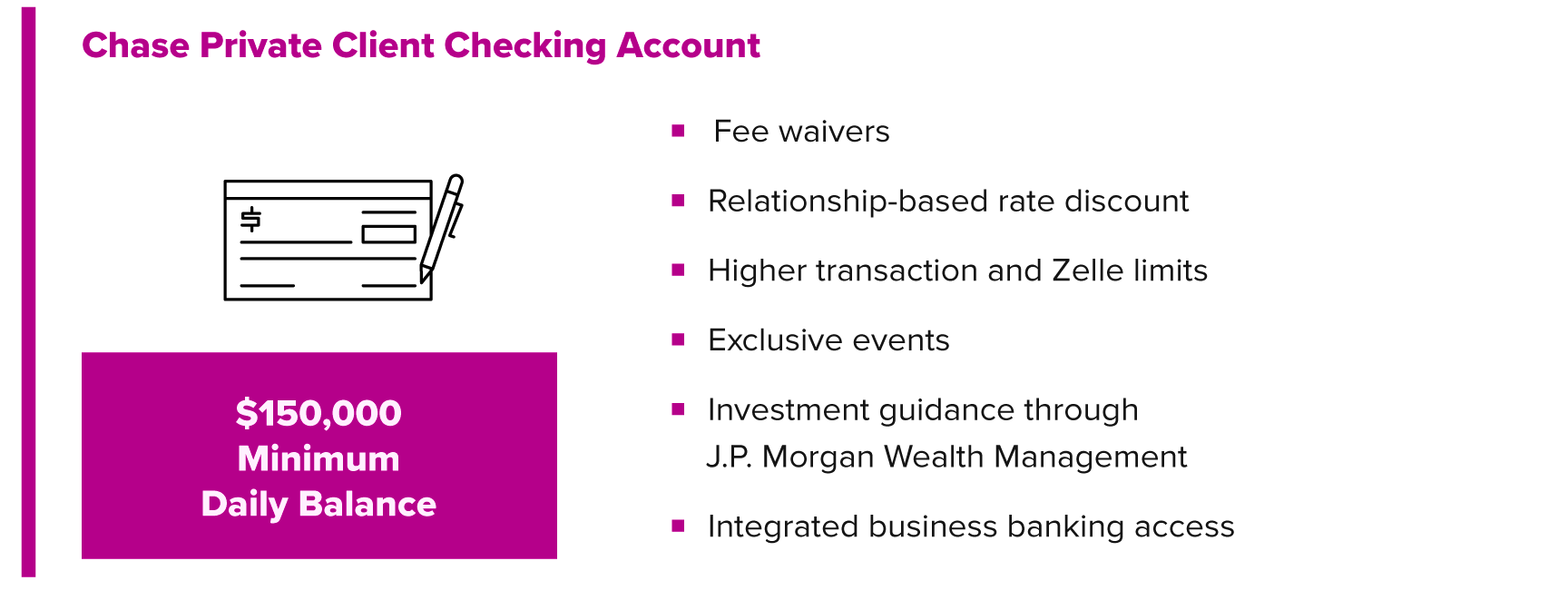

Chase has built one of the clearest examples of a relationship ecosystem: banking, lending, travel, wealth management, and premium rewards are designed to reinforce one another. The Chase Private Client Checking account illustrates how features are bundled to deepen relationships rather than provide standalone product value marketed as a personalized financial relationship.

The value comes less from any single feature and more from how the features work together to deepen engagement across the ecosystem.

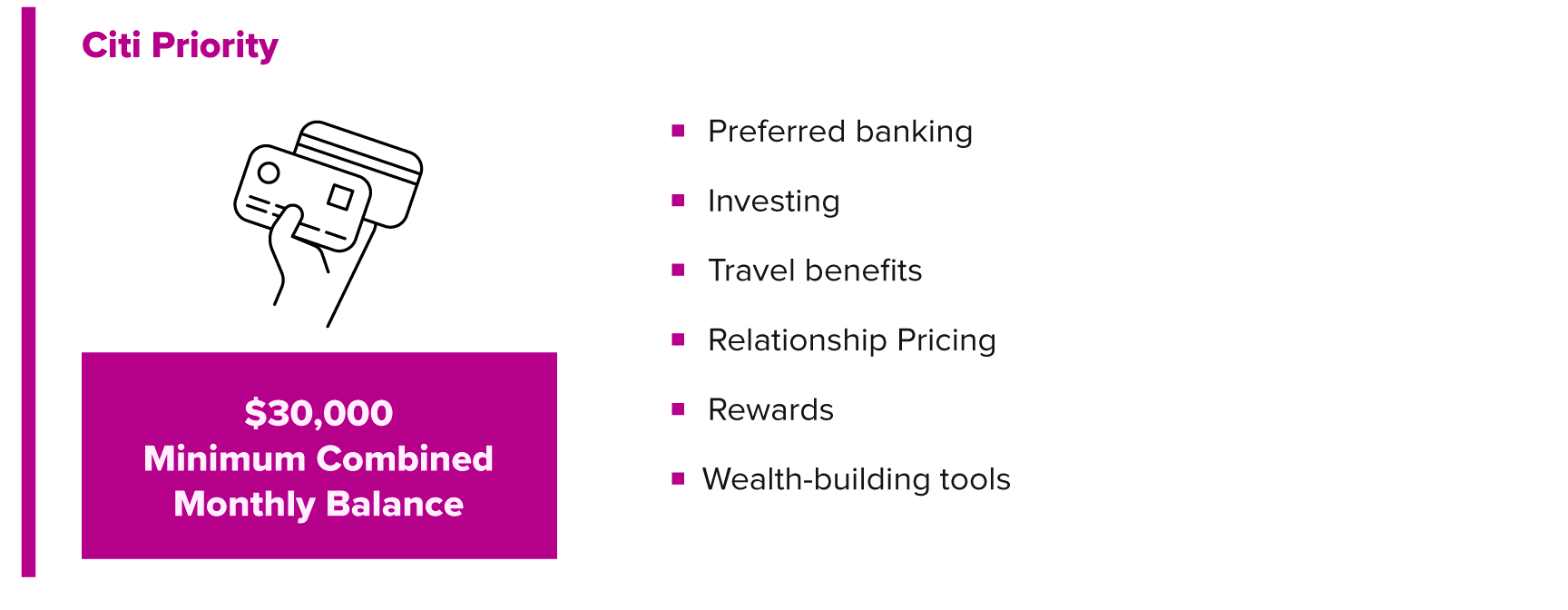

Citi demonstrates a similar strategy, though with even stronger emphasis on rewards optimization, tiered relationship banking, and lifestyle integration. Products like Citi Priority position banking as an entry point into a broader ecosystem.

As balances and engagement increase, members unlock additional benefits including waived fees, higher limits, commission-free trading, investment tools, travel perks, and pricing discounts.

Again, the individual features themselves are increasingly common across the industry. The differentiation comes from how Citi integrates them into a system designed to reward consolidation and deepen financial engagement over time.

Across both institutions, features and functionality operate less as isolated product attributes and more as mechanisms for ecosystem integration.

In this environment, institutions are no longer competing only on whom has the “best” features or functionality but on whose products work most effectively to create a coherent financial experience.

Differentiation Strategy #3: Emphasizing ease in consumer experience

Experience increasingly determines whether members remain engaged, trusted, and emotionally connected to an institution. As digital capabilities converge, institutions compete through intuitive, supportive, and context-aware interactions that shape how the overall experience with the financial institution feels. But it’s not just about digital experience. Financial institutions emphasizing ease see digital as just one part of an overall strategy to make people’s (financial) lives better.

Ally, for example, differentiates through low-friction digital banking that emphasizes simplicity, transparency, and confidence-building rather than financial complexity. The experience reinforces the brand promise: approachable, easy-to-use banking without unnecessary friction. Across products, simplicity, accessibility, institutive digital tools, transparency, and confidence-building financial management are consistently emphasized through the digital interface making the experience itself part of the product value proposition. Even its language reinforces the experience design: "Technology and humanity can coexist." "Everything we do is by humans, for humans." "Straightforward with no surprises.".

Navy Federal’s experience strategy takes on a different approach, centering on trust, support, and understanding military life transitions. While the digital experience matters, this experience view is more holistic. Across products, the institution reinforces reliability, member advocacy, and long-term relationship support rather than transactional optimization alone. Examples include:

- Early direct deposit for active-duty service members,

- Flexible deployment-related support,

- Military-specific lending products, and

- Language that reinforces reliability and service.

The experience communicates: “This institution understands the realities of military life,” and emotional connection that is difficult to replicate through features alone.

Building Differentiation around Member Realities

This analysis is the beginning of a broader focus on products and experience in Filene's Center of Excellence for The Next Generation of Member Growth, but the early findings show that the complexity of individual products and product portfolios is rising. The ubiquity of certain features has changed differentiators into table stakes and shifted differentiation upstream into more complex and integrated strategies.

Differentiated product value is now being derived from holistic views into what the financial institution can deliver and what the consumer needs. These products signal to the consumer who the institution is built for, what it understands about their lives, and how it creates value for them. These signals are essential for consumers to cut through the noise of product offerings and build a deeper relationship with their financial institution.

On the institution’s side, delivering a differentiated product portfolio requires clarity and discipline. The examples highlighted in this article are not successful because they added more features or marketed themselves as equally relevant to everyone. Their success came from making intentional choices: who they are best positioned to serve, which financial realities they are built to address, and how consistently their products, messaging, and experience reinforce that focus.

Credit unions were designed with specific members in mind. They were built to co-exist with the members they serve and be intimately familiar with their needs. They never had to define who they were or who they served; it was built-in. For many credit unions, this one-to-one mapping of institution is no longer a reality and hard decisions need to be made. Who are you as an institution and who are you not? Who are you best positioned to serve and who are you not? In a market where individual features, and even entire products, are increasingly interchangeable, to stand out your institution must create a set of products that work together in ways that are coherent, purposeful, and unmistakably built for the people they serve and the realities of their lives.

The analysis looked the following institutions:

- Digital Banks (Ally, SoFi)

- Large National Banks (Chase, Bank of America, Wells Fargo, Citi)

- Credit Unions (Navy Federal, SECU, PenFed, and SchoolsFirst FCU)

We pulled all consumer products in the following areas:

- Banking (checking and savings)

- Lending (personal, home, auto)

- Credit Cards

We documented the following for reach product:

- Product name

- Tag line

- Elevator pitch

- Rates and fees

The analysis, assisted by GenAI, evaluated products through three lenses:

- Positioning & Language: how products are named, framed, and marketed

- Features & Functionality: rates, pricing, rewards, access, and capabilities

- Experience: usability, convenience, emotional resonance, and ecosystem integration