This may seem obvious, but the U.S. payments environment is changing quickly. Members expect payments that are fast, reliable, intuitive, and fully integrated into their digital lives. Dr. Lamont Black, Filene’s Fellow for our Center of Excellence on The Credit Union of the Future, has proposed using a “SIMPLE” framework to think about payment shift.

The SIMPLE framework lays out six forces shaping this reality: Social, Invisible, Mobile, Personal, Live, and Empowered. These shifts are not theoretical. They are visible today in countries that have already modernized their payment systems at scale. By studying international examples, we can understand what a future-ready American system may look like and how credit unions can adapt.

The global perspective matters. Other nations have modernized through deliberate policy, public-private collaboration, and user-centered design. The result is a set of mature, interoperable, real-time ecosystems that show what is possible when payments become an engine for inclusion and convenience. These examples help illuminate a future state where speed, interoperability, and accessibility are standard expectations in the United States rather than emerging features.

The thoughts included here come from two pieces of Filene Research, which Filene members can read in full by clicking the links below.

SIMPLE Payments: Six Consumer Payment Trends Credit Unions Must Embrace

Global Payment Innovations: A Research Brief for U.S. Credit Unions

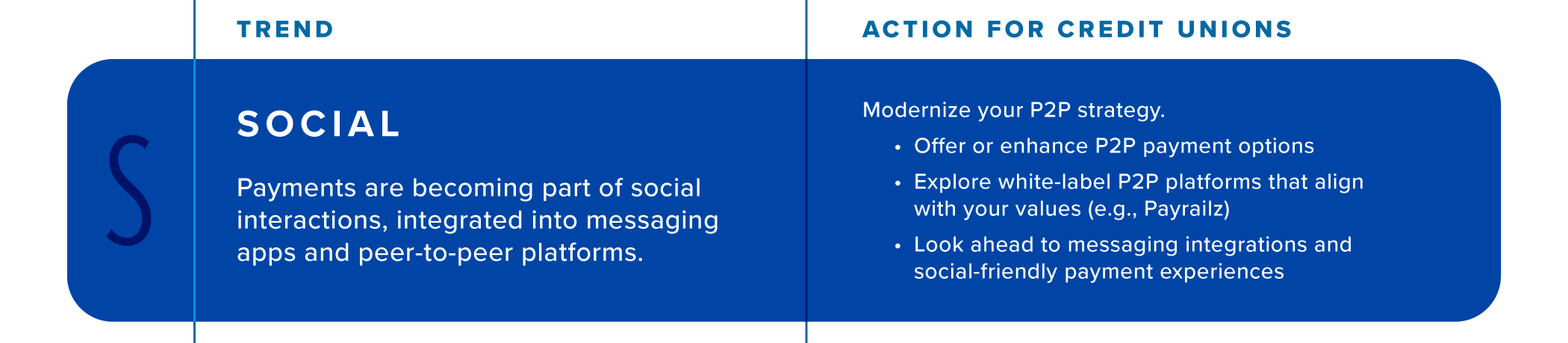

Social Payments: Where Conversation and Money Intersect

Social payments have become a default behavior. Peer-to-peer (P2P) tools are now used more often than cash for consumer-to-consumer transfers, with 64% of US consumers using them. What is interesting is how payments are now part of conversation threads, message apps and group texts, not separate transactions.

International systems demonstrate how deeply social payments can be embedded into daily life.

- Sweden’s Swish is a mobile payment platform created by major banks and the Swedish central bank that enables instant person-to-person and person-to-business payments using only a mobile number. It now processes more than one billion transactions per year and is used by most of the population.

- Brazil’s Pix, designed and mandated by the Central Bank of Brazil, provides free, real-time transfers using phone numbers, national IDs, email addresses, or QR codes. Roughly 76 percent of Brazil’s population uses Pix, making it the dominant payment method across income levels and regions.

Key takeway for credit unions: Modernize your P2P strategy. These systems show what happens when fast, interoperable payments become mainstream: people stop thinking about “payments” as a task and treat them as a communication tool.

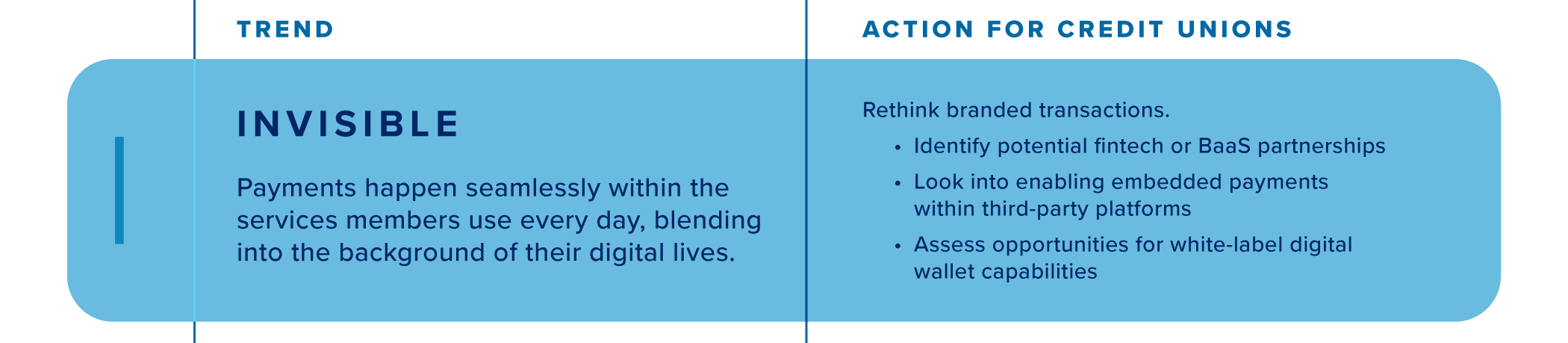

Invisible Payments: When Payments Move Into the Background

Invisible payments happen when financial transactions are absorbed into everyday digital experiences. Subscription platforms, ride-share apps, and e-commerce checkouts have demonstrated how seamless this can be. Credit unions have been active in embedded finance for years (think indirect lending), but now that space is even more seamless.

Globally, invisible payments are even more advanced.

- India’s Unified Payments Interface (UPI) is a government-led real-time system that links multiple financial institutions, merchants, and users through a standardized, open API structure. UPI processes more than 18 billion transactions per month and allows payments directly from bank accounts across apps without cards or intermediaries.

- China’s payments ecosystem integrates payments directly into digital platforms like WeChat Pay and Alipay. These systems handle more than 70 percent of all consumer transactions and bundle messaging, commerce, transportation, and financial services into a single continuous experience.

Key takeway for credit unions: Rethink branded transactions. Payments become “invisible” when the underlying rails are interoperable and real time.

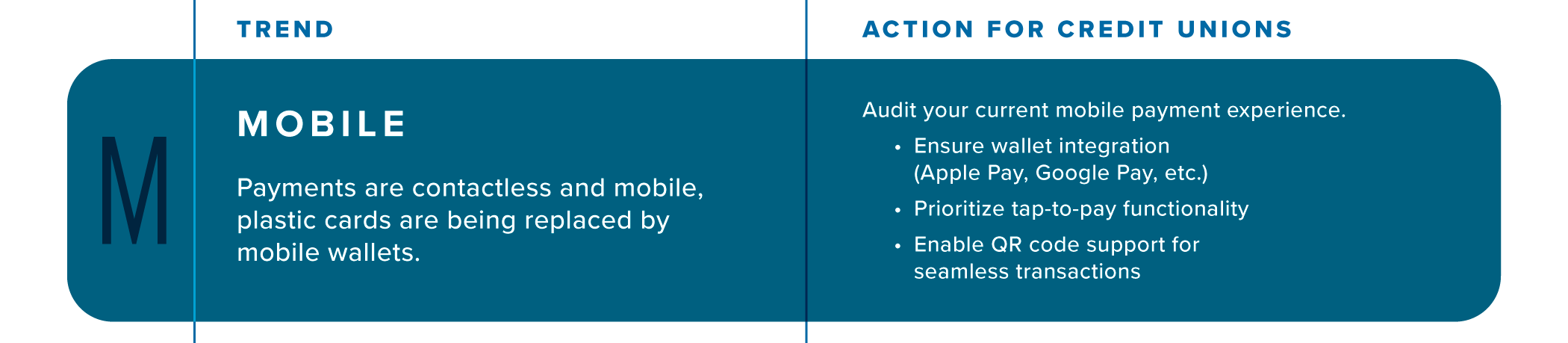

Mobile Payments: Moving to a Phone-First World

Mobile devices are becoming the primary payment instrument for younger consumers, with 80% of Gen Z shoppers preferring tap-to-pay over swiping or inserting cards. While contactless adoption and digital wallets continue to rise in the U.S., other markets are considerably further ahead, like Ireland, where contactless payments account for 87% of all point of sale card transactions.

- Costa Rica’s SINPE Móvil, operated by the Central Bank of Costa Rica, enables real-time transfers using only a phone number. It is used by 76 percent of Costa Ricans aged 15 and older and is available even through basic devices using USSD (Unstructured Supplementary Service Data) channels.

- Kenya’s mobile money ecosystem, led by M-PESA and enhanced by credit union-like SACCOs (Savings and Credit Cooperatives), has dramatically increased financial access. More than 77 percent of rural adults use mobile money services, narrowing the digital divide and enabling immediate payments even without smartphones.

Key takeway for credit unions: Audit your current mobile payment experience. Your card should be the default in your members’ digital wallet: encourage them to use it!

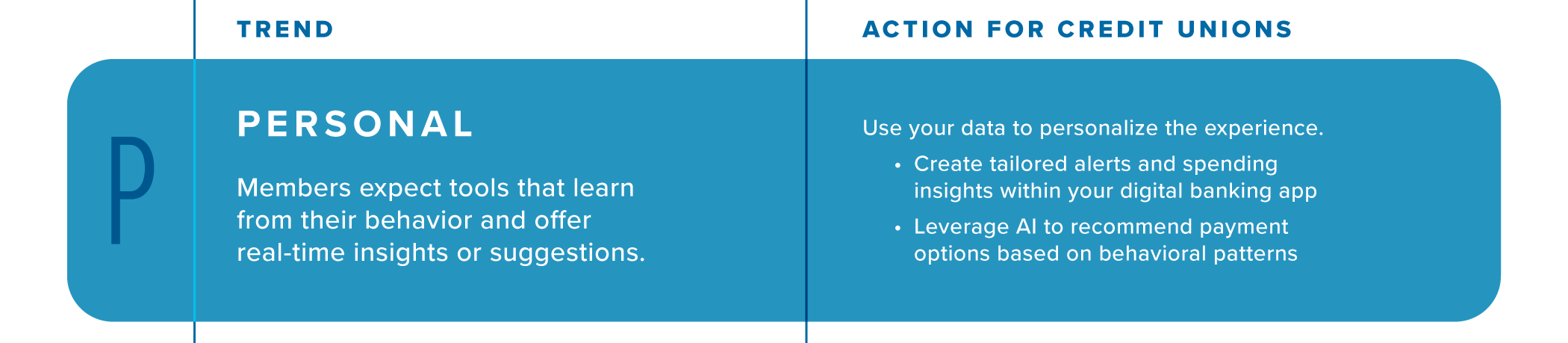

Personal Payments: Data-Driven Relevance

Personalization is becoming a core expectation. Users want financial tools that adapt to their habits and help them make informed decisions. We've found that 70 percent of consumers now expect personalized financial guidance from their institution.

Globally, many systems already incorporate this.

- In Brazil, Pix integrates strong biometric authentication, fraud detection, and refund processes that adapt to user behavior.

- In Ireland, Payac, a cooperative service platform, helps smaller credit unions personalize payment services through shared real-time payment infrastructure.

- In the United Kingdom, open banking standards allow users to share transaction data securely across institutions to enable tailored products and insights.

Key takeway for credit unions: Use your data to personalize the experience. You know which payment methods your members prefer; use that information to make recommendations based on their behavior. Also, check out Filene's Member Pulse, a segmentation tool that can help make this possible!

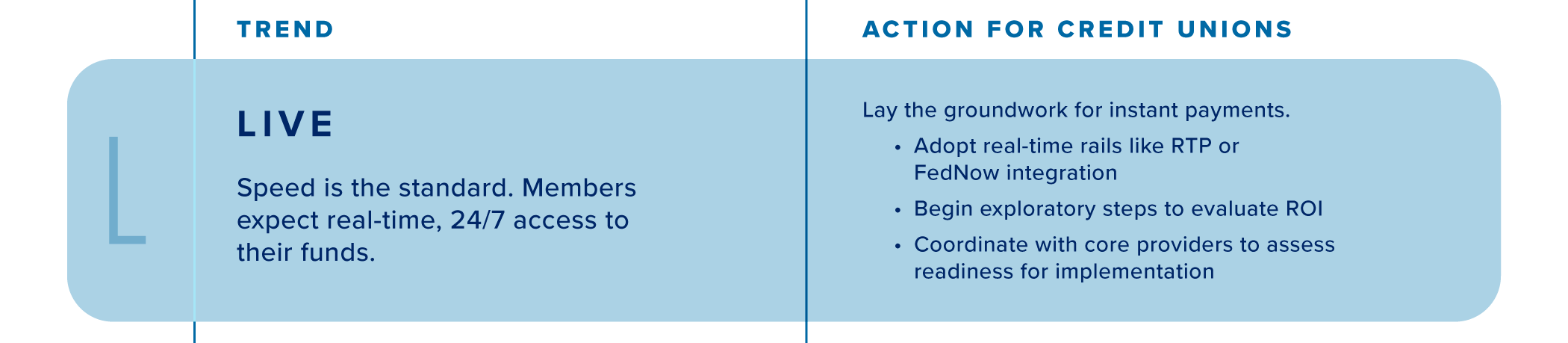

Live Payments: Real Time as the Default

Real-time payments are becoming standard worldwide. In the U.S., the Federal Reserve’s FedNow Service and The Clearing House’s Real-Time Payments (RTP) network are initial steps toward reducing settlement delays. Members already expect immediate availability of funds, and other countries demonstrate why.

- India’s UPI, Indonesia’s BI-FAST, and Brazil’s Pix all settle payments within seconds every hour of the day.

- Costa Rica’s SINPE Móvil and Kenya’s PesaLink both support immediate account-to-account transfers across institutions.

Key takeway for credit unions: Lay the groundwork for instant payments. Real-time payments strengthen trust, reduce friction, and make financial tools more usable for communities that rely on timely access to funds.

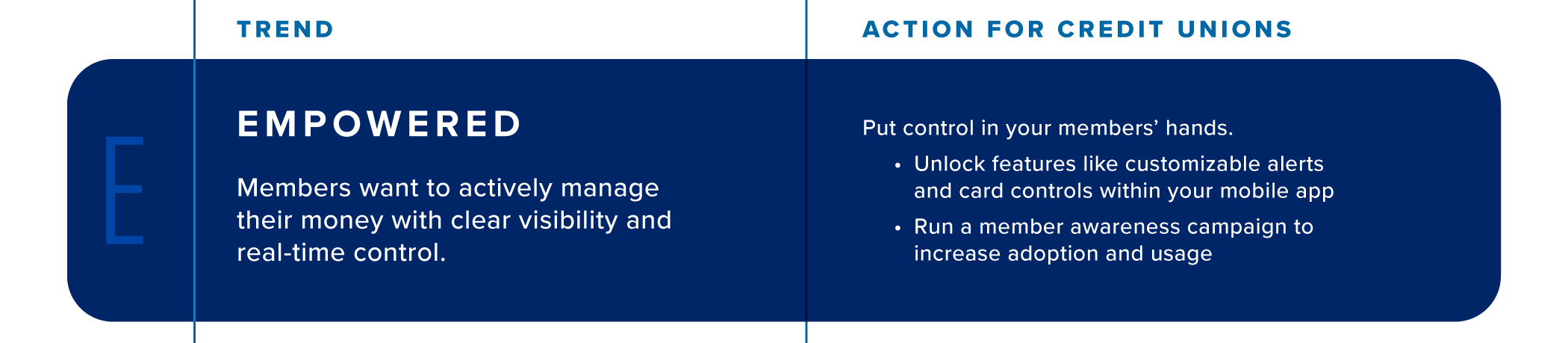

Empowered Payments: Giving Members Control

Empowered payments provide consumers direct control over their financial lives through alerts, card controls, and real-time insights. Fintech firms are setting expectations here, but global examples illustrate this shift equally well.

- In Sweden, despite being highly digital, the government still maintains physical cash resiliency for system stability, ensuring users have control even during outages.

- Indonesia’s credit union federations provide mobile apps, real-time payments, and spending tools tailored to underserved communities.

- Kenya’s SACCOs offer budgeting, loan repayment, and payment tools in mobile channels designed for low bandwidth environments.

Key takeway for credit unions: Put control in your members’ hands. Customizable alerts and card controls in the mobile app keep members in control.

The Takeaway

International systems demonstrate what is possible when payments are built around access, speed, and reliability. They show the future state the United States is likely moving toward: real-time, mobile-first, fully interoperable, and deeply embedded into daily life. Credit unions that align with the SIMPLE framework will be better positioned to deliver member value in this environment.

If your credit union is looking to take a more proactive approach to your payments strategy, we invite you to be a part of our next Center of Excellence, "All Things Payments." Set to launch in January, this is the first and only payments research center built specifically for credit unions and will help the industry navigate the quickly changing payments space. Our list of sponsors for this highly anticipated center is filling up fast - join our growing list of founding sponsors now to be a part of this revolutionary journey.

— CV