Credit unions offer important products and services for promoting financial well-being (FWB). But what does it mean to be financially well? Exploring this question may help credit unions consider new approaches, particularly among members who may be struggling financially and are motivated to do something about it.

The Financial Health Network offers the following definition of financial health, which is widely used in practice, including through the prior “Financial Well-Being for All” partnership between Filene and the National Credit Union Foundation:1, 2

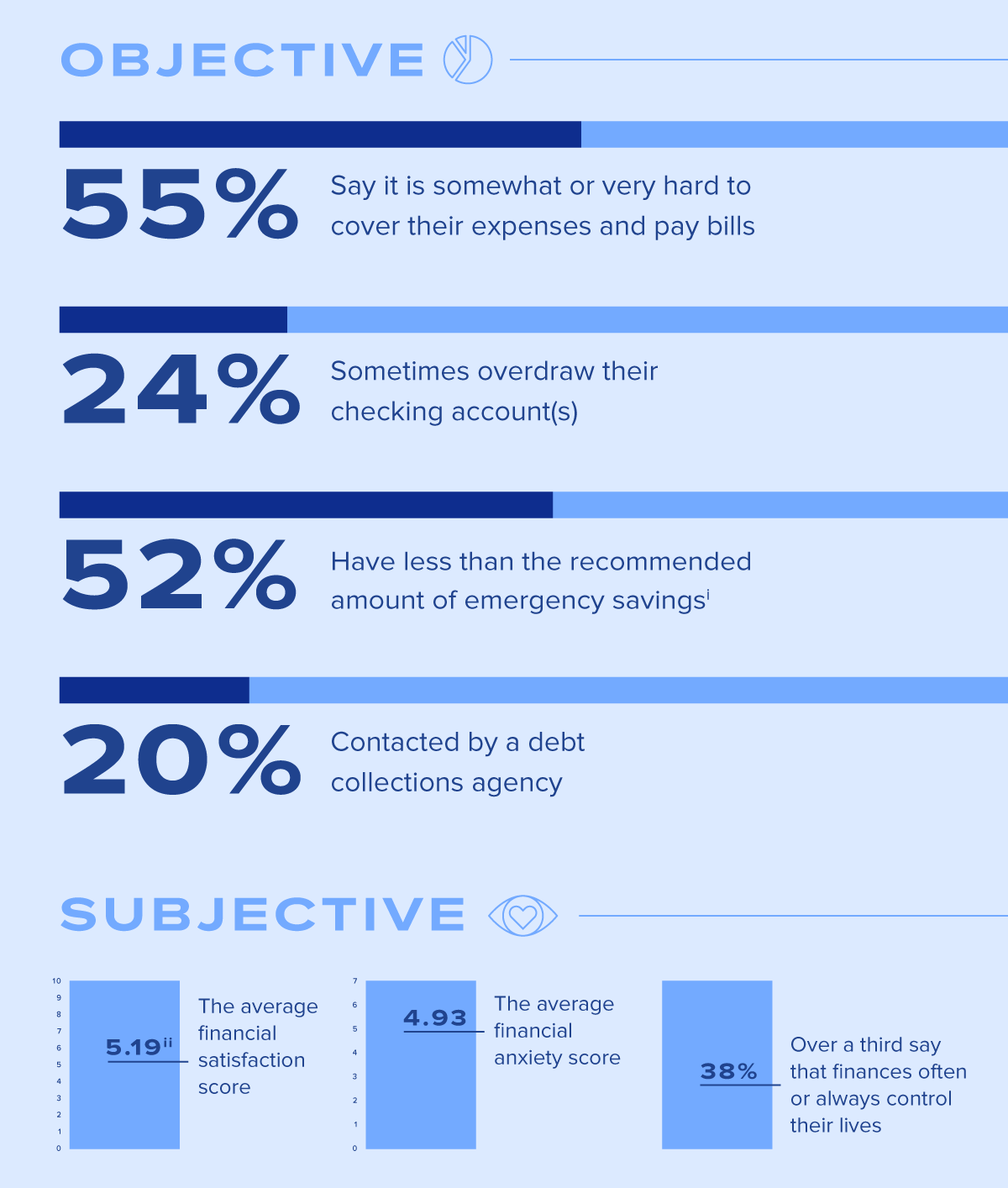

These indicators are the basis for the Financial Health Score which finds that in 2024, only 30% of surveyed U.S. households were considered financial healthy, with 53% and 17% falling into “coping” and “vulnerable” score ranges.3 According to the Financial Health Network, “Individuals who are Financially Healthy are able to manage their day-to-day expenses, absorb financial shocks, and progress toward meeting their long-term financial goals.”4

The eight indicators above offer an objective perspective on FWB—e.g., how much one has in savings, debt payments relative to income. These indicators also relate to other aspects of member well-being. For example, members whose spending is greater than their income are more likely to experience food insecurity, which is a major social determinant of health,5 and are at greater risk for eviction or foreclosure, which has many negative consequences.6 I am currently working on research that shows that those who are struggling with medical debt put off additional health care they need, which is shown to worsen health outcomes.

Subjectively, FWB can mean how one perceives and is emotionally affected by their financial circumstances and whether they feel capable of taking actions that will improve these circumstances. According to the Consumer Financial Protection Bureau, subjective FWB means feeling financially secure and having freedom of choice.7 Financial stress—worries about one’s financial circumstances—negatively impacts cognition, mental health, and relationships.8

The National Financial Capability Study (NFCS) offers perspectives on both objective and subjective FWB. Here are some highlights from my analysis of 2024 NFCS survey data from over 25,000 U.S. adults:9

Are Objective and Subjective Financial Well-Being Related?

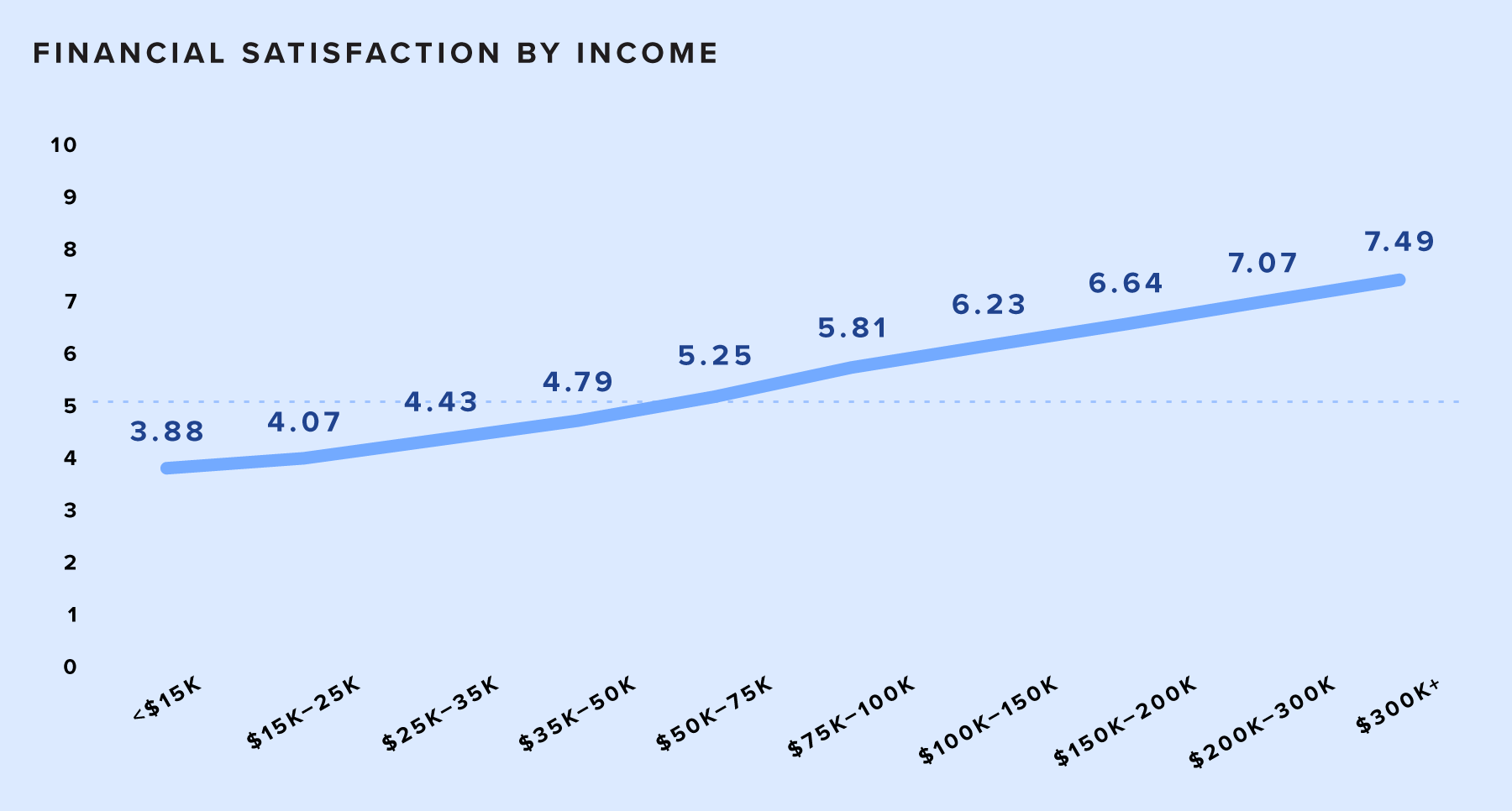

It makes sense that these two types of FWB might be related. If I struggle to pay bills on time, I probably have more financial anxiety than someone who pays their bills on time. The chart below shows a clear association between household income and financial satisfaction (the dotted red line is the average):

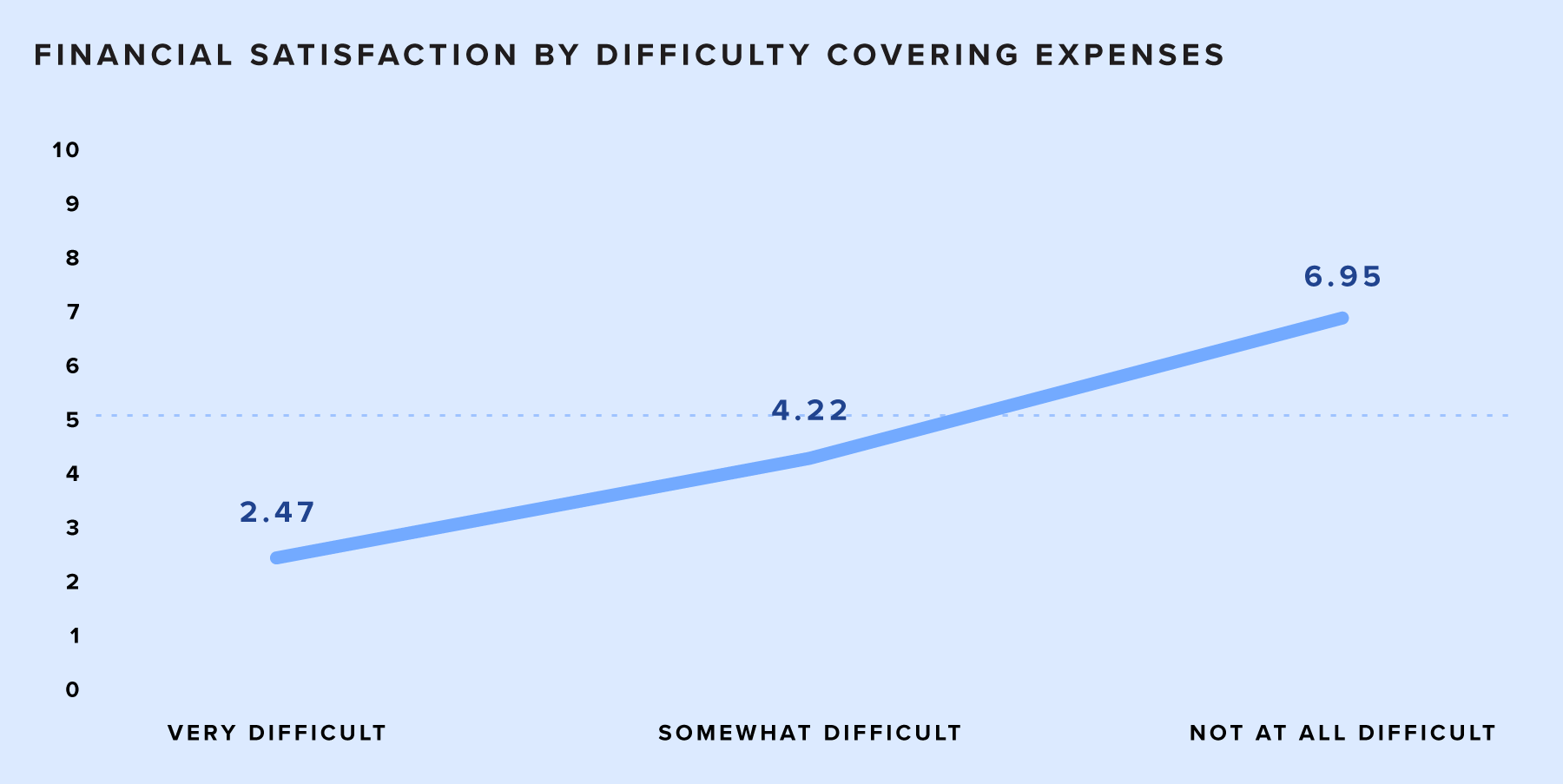

But income only tells part of the story; problems covering basic expenses also affect financial satisfaction:

Similarly, financial satisfaction scores are over three points higher among households that have emergency savings equal to three or more months of usual expenses compared to those without this level of emergency savings. I also found that problems covering expenses and a lack of emergency savings are associated with higher levels of financial anxiety.

Control is Key

The results above show us that people’s subjective assessments of their financial circumstances are generally accurate. Problems paying one’s bills is a reason to worry. Concerning both objective and subjective FWB, it is important to consider whether people feel like they are in control of their financial destinies. Among NFCS survey respondents who say their finances often or always control their lives, the average financial satisfaction score is only 3.63 compared to 6.14 for those who say finances control their lives never, rarely, or sometimes.10

The danger among people who feel like they lack financial control is learned helplessness—that there is no sense trying to manage one’s spending, save, and reduce debt because they are up against economic forces beyond their control.11 This is why conducting a budget assessment is important in financial counseling. Perhaps the reason why a member feels helpless is because their income is insufficient to cover the rising costs of housing, food, health care, transportation and more.12

The solution may not be better budgeting, but help exploring higher paying job opportunities and accessing public and community resources. Still, neither credit unions nor their members can control the cost of living and the supply of good paying jobs with benefits.

Financial Anxiety Can Help and Hurt

Financial anxiety can be good or bad. Worrying about money can motivate us to spend more wisely and save more, but only up to a point.iii Too much anxiety can impair financial decision making, especially amidst uncertainty and potential loss.13

Vibes and Uncertainty

Kayla Scanlon coined the term “vibecession” to explain the disconnect between macroeconomic indicators and how people feel about the economy.14 For example, unemployment remains under 5% and inflation has remained steady at around 3% since June 2024, yet 77% of employees are worried about the current economic climate.15

I suspect that much of this sentiment is related to the link between uncertainty and anxiety16 and whether people may experience future economic gains or losses.17 People are unsure of how their FWB might be affected by things like tariffs and changing trade relations, interest rates, artificial intelligence, and climate change. It is important to consider that though members’ objective FWB may look good today (e.g., routinely positive cash flow, regular savings deposits, and on time loan payments), they may still be worried about what their FWB may look like in 6 months.

Social and Cultural Factors

As social creatures, we look to others for cues about how to behave—what behavioral economists refer to as “social proof”.18 If we see that other people are spending within their means and saving money for emergencies, we are more likely to do the same.

Yet social comparisons can also be harmful. If we compare ourselves to those who have more income and wealth, we may feel badly about our financial situation, even if in objective terms we are doing okay—a phenomenon that is all-to-often prominently reinforced via social media.19

Subjective FWB may also be affected by different cultural values and experiences. In the NFCS data, I see that financial satisfaction is lower among those who identify as White compared to those who identify as non-Whiteiv—even when objective FWB indicators like income and savings are the same. This finding may relate to differences in how important personal finance is relative to other quality of life domains. In addition, immigration status and language differences affect perceptions and use of financial services such as basic banking and credit.20

Takeaways for Credit Unions

Financial well-being is both a set of financial circumstances and how one perceives and feels about these circumstances.

Credit unions can put these ideas into practice using evidence with various strategies for collecting and analyzing member data to better understand drivers of objective and subjective FWB and the impacts of products, services, and interventions in guiding their decision making.

Endnotes

1 Financial Health Network. 2025. “What Is Financial Health?” Financial Health Network. Accessed September 25. https://finhealthnetwork.org/about/what-is-financial-health/

2 National Credit Union Foundation, and Filene Research Institute. Putting Financial Well-Being for All into Practice. Report no. 557 (March 11, 2022). Madison, WI: National Credit Union Foundation and Filene Research Institute. Accessed September 25, 2025. https://www.filene.org/reports/putting-financial-well-being-for-all-into-practice

3 Warren, Andrew; Wanjira Chege; Kennan Cepa; and Necati Celik. Financial Health Pulse® 2024 U.S. Trends Report: Diverging Financial Health Indicators. Chicago: Financial Health Network, September 2024. Accessed September 25, 2025. https://finhealthnetwork.org/research/financial-health-pulse-2024-u-s-trends-report/

4 Ibid.

5 Office of Disease Prevention and Health Promotion. “Food Insecurity.” Healthy People 2030, U.S. Department of Health and Human Services. Accessed September 25, 2025. https://odphp.health.gov/healthypeople/priority-areas/social-determinants-health/literature-summaries/food-insecurity

6 Desmond, Matthew. Evicted: Poverty and Profit in the American City. New York: Crown Publishers, 2016. “Evicted – Matthew Desmond” (official site). Accessed September 25, 2025. https://evictedbook.com/

7 Consumer Financial Protection Bureau. “Why Financial Well-Being?” Consumer Finance. Accessed September 25, 2025. https://www.consumerfinance.gov/consumer-tools/financial-well-being/about/

8 Peetz, Johanna. “What Financial Stress Does to Relationships.” Psychology Today, August 21, 2024. Accessed September 25, 2025. https://www.psychologytoday.com/us/blog/financial-matters/202405/what-financial-stress-does-to-relationships

9 FINRA Investor Education Foundation. National Financial Capability Study (NFCS) 2024 State-by-State Survey. Washington, DC: FINRA Investor Education Foundation, 2025. Accessed September 25, 2025. https://finrafoundation.org/national-financial-capability-study

10 Ibid.

11 “Learned Helplessness.” Psychology Today. Accessed September 25, 2025. https://www.psychologytoday.com/us/basics/learned-helplessness

12 Lowrey, Annie. “The Great Affordability Crisis Breaking America.” The Atlantic, February 7, 2020. Accessed September 25, 2025. https://www.theatlantic.com/ideas/archive/2020/02/great-affordability-crisis-breaking-america/606046/

13 Hartley, Catherine A., and Elizabeth A. Phelps. “Anxiety and Decision-Making.” Biological Psychiatry 72, no. 2 (July 15, 2012): 113-118. doi:10.1016/j.biopsych.2011.12.027. Accessed September 25, 2025. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3864559/

14 Scanlon, Kyla. “The Vibecession: The Self-Fulfilling Prophecy—Are We Manifesting a Recession?” The Kyla Substack, June 30, 2022. Accessed [Date You Accessed]. https://kyla.substack.com/p/the-vibecession-the-self-fulfilling

15 Bank of America. 2025 Workplace Benefits Report. Charlotte, NC: Bank of America, August 26, 2025. Accessed [your access date]. https://business.bofa.com/content/dam/flagship/workplace-benefits/ID22-0888/2025-WBR.pdf

16 Grupe, Daniel W., and Jack B. Nitschke. “Uncertainty and Anticipation in Anxiety: An Integrated Neurobiological and Psychological Perspective.” Nature Reviews Neuroscience 14, no. 7 (July 2013): 488-501. Accessed September 25, 2025. https://europepmc.org/articles/PMC4276319

17 Gal, David, and Derek D. Rucker. 2018. “The Loss of Loss Aversion: Will It Loom Larger Than Its Gain?” Journal of Consumer Psychology 28 (3): 497-516. doi:10.1002/jcpy.1047.

18 National Academies of Sciences, Engineering, and Medicine, Division of Behavioral and Social Sciences and Education, Board on Behavioral, Cognitive, and Sensory Sciences, Committee on Future Directions for Applying Behavioral Economics to Policy, eds. Behavioral Economics: Policy Impact and Future Directions (Washington, DC: National Academies Press, 2023), chap. 4, “The Behavioral Economics Toolkit: Policy Levers and Intervention Strategies.” Accessed September 25, 2025. https://www.ncbi.nlm.nih.gov/books/NBK593511/

19 Verduyn, Philippe; Nino Gugushvili; Karlijn Massar; Karin Täht; and Ethan Kross. “Social Comparison on Social Networking Sites.” Current Opinion in Psychology 36 (2020): 32-37. doi:10.1016/j.copsyc.2020.04.002. Accessed September 25, 2025. https://www.sciencedirect.com/science/article/pii/S2352250X20300464

20 Ballard, Jaime, Elizabeth Wieling, Catherine Solheim, and Lekie Dwanyen, eds. Immigrant and Refugee Families, 2nd Ed. “4.3 Financial Problems.” In Pressbooks edition. Minneapolis, MN: Open Textbook Library / University of Minnesota, 2019. Accessed September 25, 2025. https://open.lib.umn.edu/immigrantfamilies/chapter/4-3-financial-problems/

21 Capellan, Chris. “Lessons from a Financial Coach: Prioritize Expenses, Identify Resources, and Make a Plan.” Neighborhood Trust Financial Partners, September 18, 2020. Accessed September 25, 2025. https://neighborhoodtrust.org/2020/09/18/lessons-from-a-financial-coach-prioritize-expenses-identify-resources-and-make-a-plan/

i Three months’ worth of usual household expenses.

ii 1 = not at all satisfied to 10 = extremely satisfied

iii https://www.healthline.com/health/yerkes-dodson-law#stress-performance-bell-curve

iv The publicly available NFCS dataset only includes race/ethnicity categories of “White” and “non-White”.