Without a doubt, the top question I have heard from credit unions thus far is “How can we measure financial well-being?” Credit unions want to know how to better understand their members’ financial well-being and whether their efforts to improve it are having an impact. As I wrote about in the second blog of this series, there are objective and subjective aspects of financial well-being. The objective aspects offer a basic framework to organize data indicators by sources of data, including surveys, transaction and loan accounts, and credit reports as reflected in Table 1 below:

An important thing to note about the table above is that some indicators reflect a financial behavior (e.g., paying credit card balances in full each month) while others reflect a financial condition (e.g., a savings account balance). Also, these data sources have certain limitations. Collecting survey data has its challenges. Survey response rates can be low and members who respond may not be representative of a credit union’s membership. Also, respondents may not answer questions about their financial behavior or conditions accurately. Conversely, account and credit report data are direct observations of financial behaviors and conditions and free of measurement error and sample selection bias, plus these data can be used to track financial well-being over time (e.g., average monthly net savings deposits over a 12-month period). However, credit reports sometimes contain inaccuracies and transaction accounts do not necessarily reflect a household’s full set of inflows and outflows, whereas in surveys, we can ask respondents to report on financial conditions for the entire household.

The indicators in Table 1 can be used for benchmarking, e.g., survey responses of your members compared to state and national samples, member credit indicators relative to other credit unions with similar characteristics and/or the geographic area served by the credit union. Transactions can be used to calculate common ratios with standard thresholds, e.g., a liquidity ratio (liquid assets/monthly expenses) of 3.0 corresponds to standard personal finance advice of having liquid savings equal to three months’ worth of living expenses.

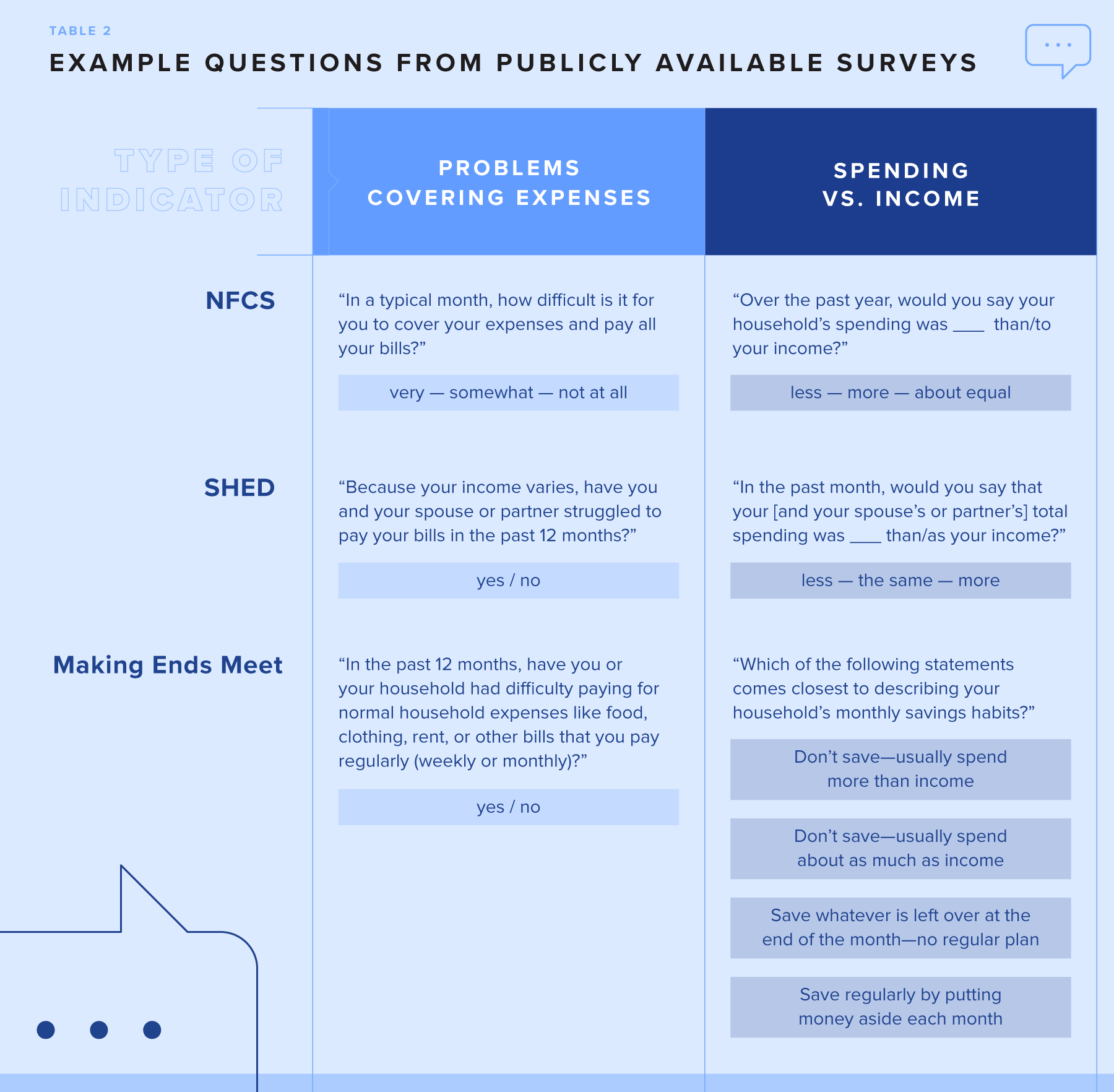

Credit unions do not need to design their own surveys to capture the indicators in Table 1. There are existing publicly available surveys with questions that reflect these indicators. Some examples are the National Financial Capability Study (NFCS) surveyi, the Survey of Household Economics and Decisionmaking (SHED)ii, the Making Ends Meet surveyiii, and the Financial Well-being Scaleiv; Table 2 showcases how some of their questions differ. Generally, items from publicly available survey questionnaires can be used for non-commercial purposes with proper attribution.

To measure subjective financial well-being, the Consumer Financial Protection Bureau’s (CFPB) Financial Well-Being Scalev is used widely by practitioners and researchers and comes with a handy scoring guide. One item I especially appreciate is “My finances control my life” (Always/Often/Sometimes/Rarely/Never) because it reflects an individual’s financial locus of control—the extent to which they feel they can take actions that can affect their financial well-being versus being affected by factors beyond their control.vi

One item I especially appreciate is “My finances control my life” (Always/Often/Sometimes/Rarely/Never) because it reflects an individual’s financial locus of control—the extent to which they feel they can take actions that can affect their financial well-being versus being affected by factors beyond their control.

However, the CFPB scale does not measure financial self-confidence as clearly as I would like. For that, the Financial Self-Efficacy scalevii has a great question: “I lack confidence in my ability to manage my finances.” (Exactly true/Hardly true/Moderately true/Not at all true).

In addition to using existing survey items concerning financial well-being, it is also important to include standard demographic and household questions (e.g., age, number of children) so results can be analyzed with respect to member characteristics. Ideally, survey responses could be linked to member transaction and credit data. For example, this could help to relate self-reported challenges like problems making housing payments with cash flow characteristics or to assess whether member responses to survey questions assessing subjective financial well-being correlate with objective indicators such as liquidity and debt-to-assets ratios. When measuring objective or subjective financial well-being, it is important to remember that for some members, results reflect the influence of economic factors beyond their control, such as high housing costs.

Customizing Surveys

Existing survey questionnaires may not meet all survey measurement needs for a credit union. A clear example is when a credit union wants to understand member experiences with a particular product or service or their responses to an intervention like a savings campaign. Sometimes a credit union wants to go deeper on particular issues, like medical debt or the use of buy now pay later products. In such cases, it may be helpful to adopt a standardized “core” of questions related to Table 1’s financial well-being indicators, member demographics, and household characteristics, in addition to customized modules for specific topics or purposes. For example, a credit union may have a “core” question about types and amounts of debt, but tie in another aspect of member well-being with questions about the unique nature of medical debt and how it may affect access to health care. Keep in mind that customizing a survey may involve additional survey design expenses.

Leveraging Account and Credit Data

Credit unions sit on a treasure trove of data concerning their members’ financial well-being. If machine learning on cash flow data can improve underwriting and expand access to creditviii, imagine what credit unions could do with a financial well-being dashboard with indicators tied to member account data—not just to support a segmentation approach (e.g., Member Pulse) but to track changes in members’ financial well-being over time. Data linking is important, such as linking to credit scores from information about members with secured credit cards or linking to savings account data from readouts about members who clicked on an emailed savings campaign invite.

Member Pulse

Member Interviews: Measuring What Survey and Account Data Cannot

It is easy to think about financial well-being only in quantitative terms. Yet there are many aspects of financial well-being that surveys and account data cannot capture. A simple rule of thumb is to use interviews with members when you want to better understand the “how” and “why” of financial well-being, not just the “what.” For example, with survey, account, and credit report data, we can measure indicators about members’ ability to manage debt. But qualitative data from interviews can tell a richer story —how members’ relationships and mental health are affected by debt struggles; how members understand and perceive different options for addressing debt problems such as credit counseling, debt management plans, and debt settlement; what steps members have taken to resolve their debt problems; and more. Interviews can be especially helpful in understanding member engagement, like how members perceive and experience various products, services, and interventions; how they perceive the credit union as having resources to improve their financial well-being; and other subjective questions you might have.

Interviews can be especially helpful in understanding member engagement, like how members perceive and experience various products, services, and interventions; how they perceive the credit union as having resources to improve their financial well-being; and other subjective questions you might have.

A Few Thoughts on Measuring Impact

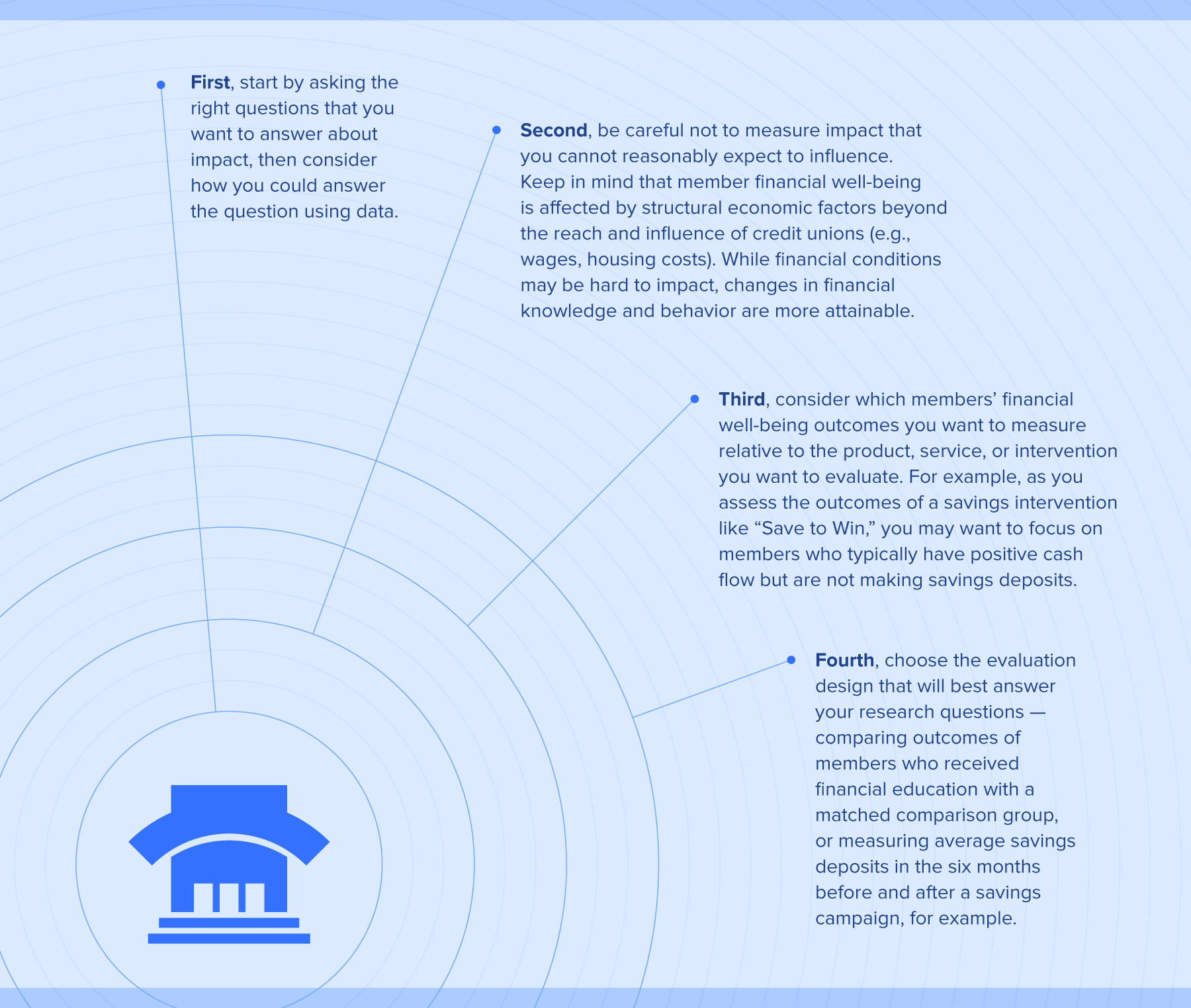

We can’t comprehensively cover measuring the impact of credit union products, services, and interventions on members’ financial well-being with data in a single blog post, but I can offer a few key tips.

Final Thoughts: Capacity, Shared Learning, and Collective Impact

Credit unions’ time and resources they have for measuring financial well-being and the impacts of their products and services will vary. The Member Well-Being Center of Excellence is an opportunity to share best practices, including how existing initiatives (e.g., Member Pulse) and partnerships (e.g., Gallup) may help, and whether and how to ask for help from outside data analytics and research firms and academic institutions. Ideally, credit unions would use a common set of financial well-being measures that could be compared with the economic characteristics of the communities they serve to demonstrate the collective impact of the credit union movement.9

Endnotes

1 FINRA Investor Education Foundation. The National Financial Capability Study (NFCS). Washington, DC: FINRA Investor Education Foundation, 2024. Accessed September 25, 2025. https://finrafoundation.org/national-financial-capability-study

2 Board of Governors of the Federal Reserve System. Codebook for the 2024 Survey of Household Economics and Decisionmaking (SHED). Washington, DC: Board of Governors of the Federal Reserve System, 2025. Accessed September 25, 2025. https://www.federalreserve.gov/consumerscommunities/files/SHED_2024codebook.pdf

3 Consumer Financial Protection Bureau. “Making Ends Meet Survey.” Accessed September 25, 2025. https://www.consumerfinance.gov/data-research/making-ends-meet-survey/

4 Consumer Financial Protection Bureau. Measuring financial well-being: A guide to using the CFPB Financial Well-Being Scale.“ Washington, DC: CFPB, 2017. Accessed September 25, 2025. https://www.consumerfinance.gov/data-research/research-reports/financial-well-being-scale/

6 “Locus of Control.” Psychology Today. Accessed September 25, 2025. https://www.psychologytoday.com/us/basics/locus-of-control

7 Lown, Jean M. “Development and Validation of a Financial Self-Efficacy Scale.” Journal of Financial Counseling and Planning 22, no. 2 (2011): 54–63. SSRN 3733862. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2006665

8 FinRegLab. “FinRegLab Study Finds Improvements in Consumer Underwriting and Credit Access from Models Using Machine Learning and Cash Flow Data.” Press release, Washington, DC, July 1, 2025. Accessed September 25, 2025. https://finreglab.org/press-releases/finreglab-study-finds-improvements-in-consumer-underwriting-and-credit-access-from-models-using-machine-learning-and-cash-flow-data/

9 For example, credit health data of members who receive loans compared with a community’s Credit Insecurity Index or loan delinquency rates compared with a community’s aggregate-level delinquency rates.